|

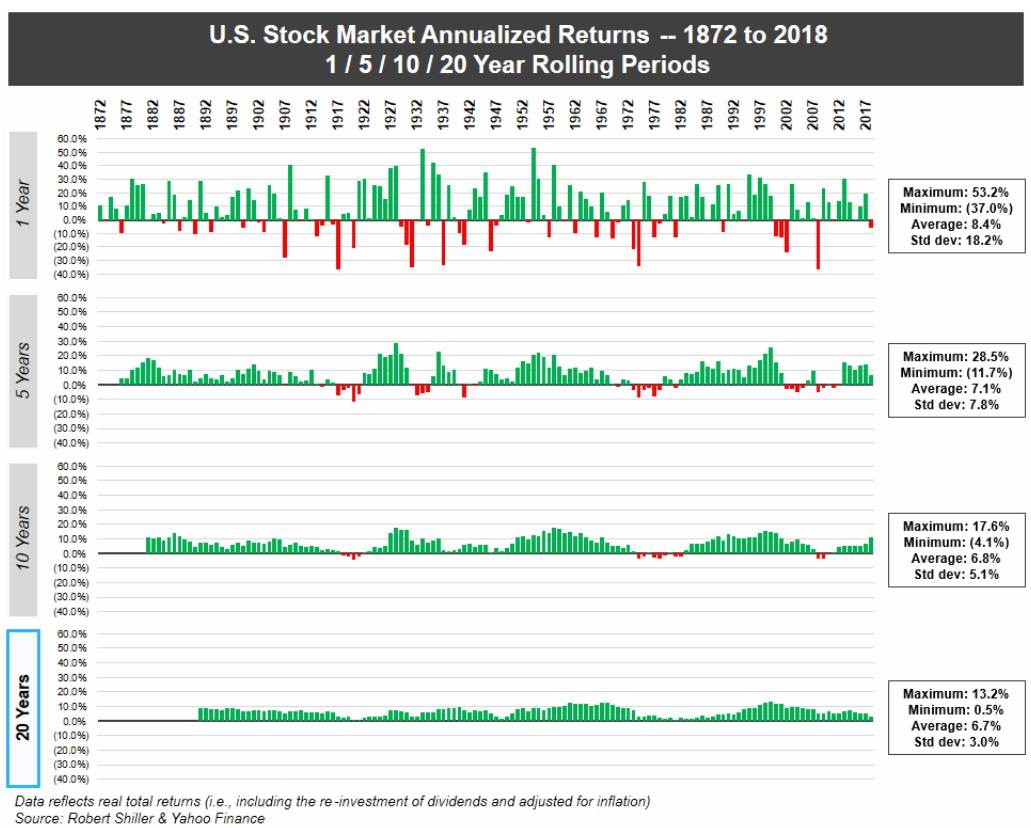

Investing in your future pretty much requires that investors have patience. I know, I know...it's easier said than done. The historical proof is in the pudding. See the chart(s) below. There has never been a 20-year period where the stock market hasn't had a positive return (although this doesn't guarantee the future will be like the past). While 1-year returns and even 5-year returns have had many periods that have had negative returns. This clearly shows that investors that are willing to accept short-term losses can reasonably expect long-term gains. While very few things in life are guaranteed and investment gains are not one of them, however, there is a high likelihood that you will be successful if you give yourself and your investments enough time. Planning for retirement, buying a new home, or saving for your child's education are important financial decisions and you can significantly put the odds in your favor of success by ignoring the short-term noise and focusing on the what the long-term can likely provide.

0 Comments

What do I mean when I'm talking about the Big One, well I'm not talking about what you might think. I'm talking about the one big mistake that would dramatically impact your life. The Big One is any event or decision that leads to an outcome that could be considered catastrophic and unrecoverable. In this article, I will be talking about financial related Big Ones, but there are many other Big Ones to avoid, it could be physical, psychological, relational, etc. Statisticians refer to this as avoiding the left tail; what they are referring to is the far-left hand side of a normal bell shape curve. The left side is typically associated with highly improbable or highly unlikely outcomes, but when they do happen, can have a major impact. Back in the late 1990s I had a friend who worked for a technology company, and if you remember the late 90s, it was a time that saw a lot of people working for technology companies, especially if you lived anywhere in California. The company he worked for was building out several co-location server farms where people could rent the servers to build their companies by not having to buy the servers themselves. My friend, being that he worked for the company, felt that he had a good idea as to the direction his company, the technology, the industry, the people, and overall felt confident about the company’s prospects. So, on top of the company stock options that he was given when he started there, he went out and purchased additional shares in the public market. Needless to say, he was highly concentrated, essentially every dollar he had was tied up in his company. Both his net worth and income were closely connected, therefore if his company did well then it was reasonable to assume that both his income and net worth (net worth = assets – liabilities) would do well. Conversely, the opposite held as well, and by the middle of 2000 with the implosion of the .com bubble my friends outlook dramatically changed as technology companies all over were struggling to survive the shock of the stock market’s drop which would later be called the bursting of the technology bubble. This had a compounding effect on my friend, as the shares he owned dropped and eventually became worthless over a few short months. In addition, he also lost his job which sent him scrambling to find another job at the same time everyone else was looking for a job. It was a 1 – 2 punch that knocked him down and almost out which took him several years to recover. His biggest saving grace was his age, at the time he was in his early thirty’s and had time to recover. Can you imagine if this happened to him later in his career? Without time to recover, what happened to my friend would have been his Big One. The reason I bring this up is that, yes being highly concentrated with your investments does have the opportunity of a huge reward, it also comes with the higher probability of a huge loss. Fortunately for my friend, he was relatively young and had many years to rebuild his asset base. Unfortunately, this isn't the case for people who are toward the end of their career and time is working against them. This event, if it happened to a person a couple of decades older could have been their Big One. Many times, time is the key determinant of whether an event could be considered the Big One. It is this idea; your advisor's primary job is to prevent you from making this type of mistake in the first place. First the good news, let's start by talking about some of the things that investors can do wrong and recover from, which fortunately are quite a few. Investors can fail to rebalance, they can own sub-optimal investments, they can be somewhat tax inefficient, they can overpay on a mortgage, just to name a few. These are all mistakes, while definitely not ideal, people can survive and might still be able to reach their goals. Many times, if the financial advisor can just keep their client from making the big mistake, they've earned every penny you pay them. While comprehensive financial planning encompasses many things, which include things like retirement planning, investment selection, asset allocation, portfolio management, college education planning, Social Security optimization, Medicare, tax planning, estate planning, risk management and insurance, one of the most important ideas is to prevent the Big One from happening. The idea is making sure that the decisions that are being made today will not wipe a person or a family out. People can come back from many sorts of small mistakes, but it's those big critical life altering decisions that you must have a zero-tolerance threshold. It can be thought of similarly as the idea in the aviation industry where anything deemed critical, has checklists and redundancies built in. The check-lists help avoid the problems in the first place by having a system in place to make sure pilots are following standard procedures. These checklists are continually updated and improved to reflect new information and data as it becomes available. This process has proven to keep passengers safe and make air travel one of the safest forms of transportation. The redundancy aspect is about having all critical systems backed up just in case the original system fails the secondary system can take over. This multi-level system builds on the idea of an industry that strives for zero-tolerance failure. This type of process and zero-tolerance of failure is exactly what is needed in your financial life. Having initial plans, contingency plans, check-lists, etc., all in the name of making sure you never get blinded-sided by the Big One. The challenge is that many clients may not realize it, but they need their advisor to be a barrier between themselves and a bad decision. How much is avoiding the Big One worth? How much is it worth in terms of stress, in terms of money, in terms of physical health, in terms of mental health, and in terms of relationships saved?  |