“What is the difference between a taxidermist and a tax collector? The taxidermist takes only your skin.” – Mark Twain The old adage, “It’s not what you make, but what you keep that matters,” is very real. As we have all heard, the only two things are certain in this world are death and taxes. Uncle Sam always gets paid. So, any way that you can legally pay less in taxes is an instant boost to your income and/or net-worth. What are some ways to optimize your After-Tax Returns? Optimize Use of Tax-Advantaged Accounts Taxes are a major drag on returns, it’s always important to consider the account in which securities are held so as to minimize current and future tax impacts. Account selection is just one of many tax-related factors that must be considered early in an individual’s financial journey. Taxable Accounts provide greater liquidity and withdrawal flexibility, but don’t carry any tax advantages. Dividends, interest, or capital gains resulting from an asset sale get taxed each time one occurs. Taxable accounts, such as brokerage accounts, are best suited for tax efficient investments, such as passively managed funds, zero-coupon bonds, or no-dividend stocks. However, there is one way to effect your tax rate, by holding investments for longer than 1-year. If you hold an asset longer than a year before selling, you are then taxed at the current Long-Term Capital Gains Rate which is currently capped at 20% which is much lower than the Ordinary Income Tax Rate of 37%. So, if you need to sell, all else being equal, selling long-term assets is most tax advantaged Tax-Deferred Accounts are funded with pre-tax dollars. Though any activity in the account — dividends, interest, capital gains — is exempt from taxes, each distribution is subject to taxation. But, contributions to tax-deferred accounts can be deducted from tax returns, thereby lowering the amount of annual taxable income. This makes tax-deferred accounts like a traditional 401(k) or IRA best for both high-income earners and tax inefficient investments. Another advantage of having assets in these accounts are that you can rebalance your portfolio as much as you’d like without triggering any taxable events. Tax-Free Accounts offer a benefit exactly as the name suggests: they are tax-free. Not only is activity within the account tax-exempt, but distributions occur sans tax as well. Because tax-free accounts like a Roth 401(k) and IRA are subject to income limits, it’s best to contribute as much as possible during periods of lower income, as well as store investments that can return the greatest amount. A Roth 401, Roth IRA, and 529 plans can be a very powerful tool for investors with extremely long-time horizons. See another article I wrote here about tax-free gains by turning $10k into $1 million using a Roth account. While is extremely difficult to avoid taxes entirely, optimizing the use of the different accounts based on your unique situation can dramatically impact how much money you actually end up with. Use Financial Metric Tools to Analyze After-Tax Returns In addition to a sale event (taxable account) or account withdrawal (tax-deferred account), investors can face additional tax liabilities due to mutual fund or ETF managers’ decision-making. Some useful metrics for evaluating funds potential tax liabilities include:

The Bottom Line Taxes are rarely clear-cut; as income levels, portfolio values, investment goals, risk tolerances, and life itself change over time—and each factor plays into tax considerations. Having said that, it is possible to plan with various “what-if scenarios” to help maximize returns under various assumptions to limit tax liabilities owed to Uncle Sam. Using these best practices for tax-efficiency with a little up-front planning can lay a roadmap for success and maximize the rewards of a well-built financial plan. -Paul R. Rossi, CFA

0 Comments

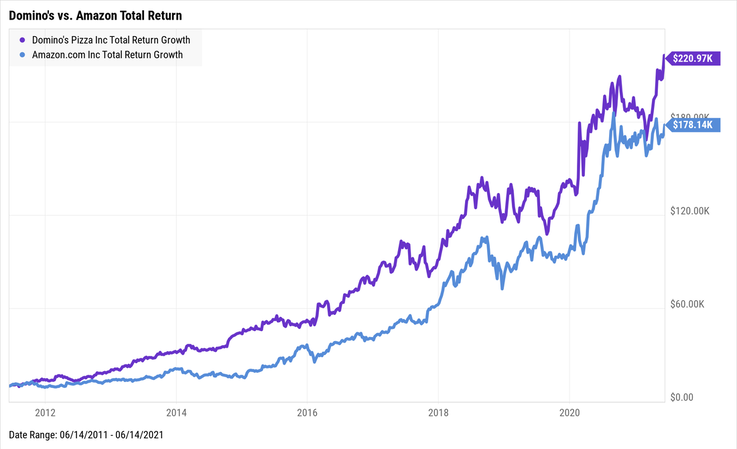

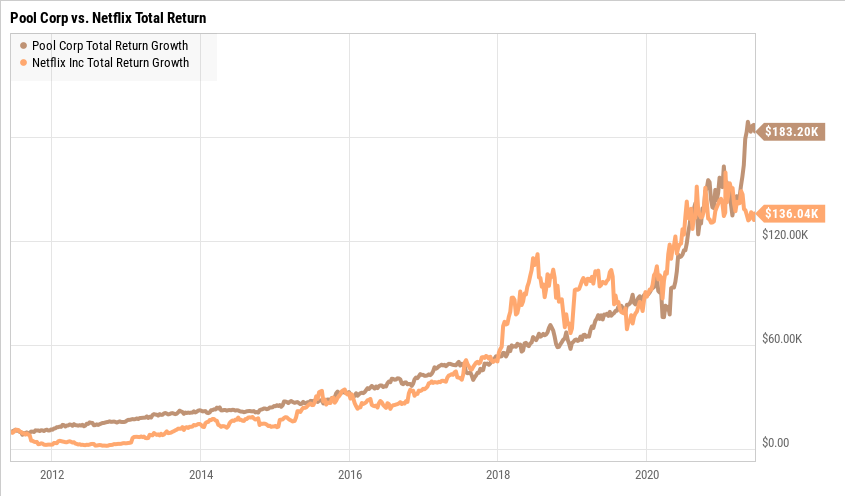

Some investors get lured into high-risk investments being told that they can make 1000%+ returns. Many times, these so-called opportunities are in very-small obscure companies, risky meme stocks, or esoteric private investments with limited or no track record. What’s interesting, is that it was possible to earn 1,000% over the last 10 years and you didn’t have to sell your soul to the devil to do it. Nor did you have to be invested in one of the FAANG (Facebook, Amazon, Apple, Netflix, Google) companies. And yes, if you were invested in these companies and held for the last 10 years, you would have done quite well. But these were not the only companies that did well. There were opportunities abound in all sorts of companies with historically strong fundamental track records. Many of these companies are household names. Can you believe that Domino’s pizza generated a 2,120%+ return over the last 10 years? In fact, this beats Amazon’s 1,760% return? So, let’s put this into real terms, $10,000 invested in Domino's 10 years ago is now worth over $220,000.  How about investing in a wholesale pool distribution company that dramatically out-performed Netflix? Pool Corp did just that, they turned $10,000 into $183,000 vs. Netflix’s $136,000.

Would you think that Mastercard or Visa would have outperformed Apple over the last 10 years? Well, they both did. Mastercard turned $10,000 into $144,000, Visa grew to 131,000, and Apple $130,000. So the next time you read an article or a friend talks about some unknown company with unproven technology that suggests there is a huge opportunity, you might pause and think about all the risk that comes with investing in something you don’t know or don’t understand. Then consider researching companies you are already familiar with that have a long runway in front of them and realize the future returns can be quite substantial, and I would argue, less risky. Below is an abbreviated list of some of the other companies that generated outsized returns for their investors over the last 10 years.

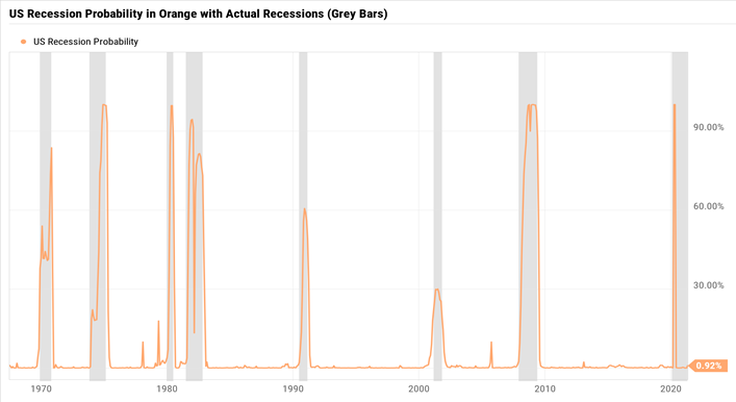

There were 39 companies in the S&P 500 that generated 1,000+ returns over the last 10 years. 38% of which were technology companies, 18% were financial services, 15% were consumer cyclical and 15% in the industrial industry. So is it possible to generate 100% returns? The short answer is yes. Is it easy? The short answer is no. So how do you do it? That’s where independent research, thoughtful analysis, and maybe just a bit of luck comes into play. -Paul R. Rossi, CFA Just so the math is clear, a 1,000% return = 10x your original investment and over a 10 year period which equates to an annualized return of 25.89%. Future Value Formula is FV = PV * ( 1+r )^t  I'm not sure anyone can accurately predict recessions, the stock market, or anything else with 100% certainty...especially when it involves human interaction, but looking at key economic data might be able to provide some measured insight as to what the future may hold. Professor Jeremy Piger of the University of Oregon maintains a recession model that might just be able to do just that...provide some probabilistic numbers to what the economy might experience in the near-term. The chart below shows the last 50+ years of U.S. recessions (grey bars). In addition to the grey bars, the orange line is what the professor has produced, called the, "U.S. Recession Probabilities" (Chauvet and Piger) which uses smoothed probabilities of a recession in the U.S. It is calculated from a dynamic factor Markov-switching model using four economic inputs:

Over the last 50 years, the U.S. has experienced 8 recessions, including our most recent 2020 Covid recession. My personal prediction is that we will continue to experience recessions going forward...so if nothing else, get used to hearing that another recession is just around the corner, because it probably is. And if the last 50 years is any guide, we can expect a recession about every 6 to 7 years. While I don't advocate jumping in and out of the market based upon recent headline news, I do believe understanding where we are in the economic cycle can be valuable for a number of reasons. Here are just a few:

While there is no absolute silver bullet to forecasting certainty, the "U.S. Recession Probability" model is a bullet none-the-less, and it never hurts to have another tool in the tool belt. -Paul R. Rossi, CFA Click here to go to Dr. Piger's website and the Recession Probabilities Model.  Many people tend to think of the 529 Education Savings Plan as a good way to save for their children's or grandchildren's education. And they'd be right. But that's where it ends for most people...and this is a potentially costly oversight. It can be much more powerful than that. So what is the 529 and how does it work? A 529 is a tax-advantaged savings plan designed to help pay for education. How does it work? The plans are funded with after-tax dollars, but all money taken out, which includes all the investment gains, are tax-free as long it is spent on qualified education expenses, expenses like: tuition, administration fees, books, room and board, computer, internet access, lab fees, etc., the list is quite extensive. Even for modest savers, the growth in a 529 account which grow tax free can easily equate to tens of thousands of dollars or more of additional money if set up and used properly. How much can you contribute? You can contribute up to $15,000 (the annual gift tax limit) per beneficiary per year. So for a couple, that would be up to $30,000 per year. However, the law permits each account owner to pay up to five years’ contribution upfront without triggering gift taxes, which means a couple can contribute up to $150,000 per beneficiary in one fell swoop. Wow. This $150,000 can then grow tax free every year. In addition to this, there is no limit to the number of 529's a person or couple can set up. A couple with a large family, say with 10 grandchildren could set aside $1.5 million (10 accounts x 150,000 max contribution). This $1.5 million is then excluded from their estate for taxes purposes - which can have a dramatic impact. What happens if money is taken out for non-qualified expense or the original beneficiary (child/grandchild) doesn't go to college? The law permits the account holder to change beneficiaries as desired without penalty. This can be used should the original beneficiary not use the money. As an example, the beneficiary account could be transferred from child #1, to child #2, to grandchild #1, etc. So in essence, you can move money across generations without taxes as long as you don't hit gift tax exclusions. That's a potentially powerful estate planning tool. However, the power of the 529 account can still be very useful if the beneficiary doesn't use the money for educational purposes. While there is a 10% penalty and taxes are due for amounts taken out for non-educational purposes, even factoring this in, the math shows the 529 account balances can be worth tens of thousands or more than simply putting the money into a regular brokerage account. Some other notable highlights:

Although 529 plans have been around for years, many people do not appreciate the flexibility they offer. While it's a great savings tool for educational purposes, the accounts can be much more than that...it can be a part of a well thought out estate plan. - Paul R. Rossi, CFA |