Investing can be stressful, but it doesn’t have to be. If you have a well-built portfolio, understand what you own, and have a plan, then you shouldn’t be too worried about market volatility and what the financial pundits are saying. Here are a few tips to help you invest wisely and stay sane at the same time.

Hopefully, taking a step back from your investing life gives you greater peace of mind and lets you focus on family, friends, your personal goals and living a fulfilling life. -Paul R. Rossi, CFA

0 Comments

First, let's ask, what is a Registered Investment Advisor?

And what makes this advisor different from a Registered Representative who works at my bank or a national brokerage firm? - A lot actually, keep reading. A Registered Investment Advisor (RIA) is a professional independent advisory firm, that is held to the highest standard of care, the Fiduciary Standard - Registered Representatives at banks and brokerage firms are not. RIA's provide personalized financial advice to their clients, many of whom have complex financial needs. Because these advisors are independent, and are required to work in their client's best interest they are not tied to any particular family of funds or investment products, so they can use the investment that is best for the client. On the other hand, If you've ever worked with a Registered Representative from one of the large firms (Wells Fargo, Morgan Stanley, Merrill Lynch, Edward Jones, etc.) you might have noticed that many of the investments (mutual fund or ETF) in your portfolio have the same names as where the advisor works. Coincidence? Nope. Morgan Stanley makes more money if a Morgan Stanley Registered Representative uses Morgan Stanley investments in their clients portfolios - to the detriment of their clients. Most importantly, they don't have to work in your best interest. Huh, how is that you ask? Well, it's the way the Wall Streets rules have been set up. They will work in their best interest, not yours and it's completely legal, and in my mind completely wrong. To make matters even more confusing, Registered Representatives at these large firms can have titles such as Advisor, Financial Advisor, Financial Planner...but in fact, legally they are just Registered Representatives of the firms they work for. As a Independent RIA (Registered Investment Advisor) and working under the fiduciary standard, Rossi Financial Group is held to the highest standard of care—and we are required to act in the best interests of our clients at all times. Period. So what are the benefits of working with an Independent Registered Investment Advisor?

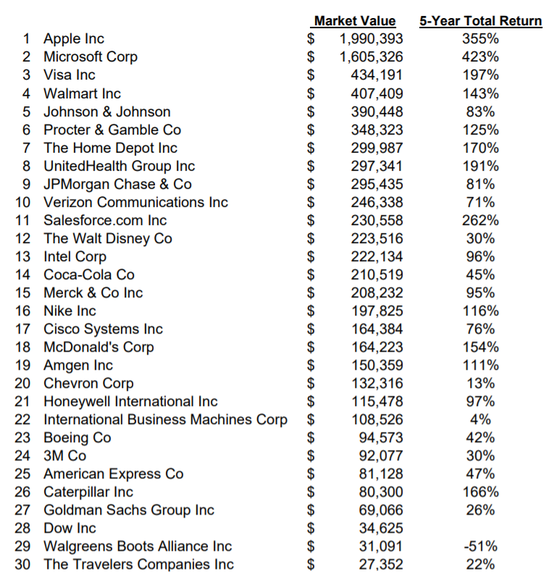

These 5 distinct benefits can make a dramatic difference in your overall financial well being. While I have a strong opinion about what type of firm you should work with, it doesn’t change the facts. So read, research, and ask a lot of questions before you enter into any financial relationship. In fact, I would require anyone you work with to sign a Fiduciary Pledge that explicitly states they will always work in your best interest. We sign one for every client. -Paul R. Rossi, CFA  Are you considered clairvoyant? Do you win an office football pool every year? Can you accurately and consistently predict 10 coin flips in a row? Are you a palm reader? Are you the sort of person who, while possessing no psychic abilities, does not mind spending hours crunching numbers and analyzing obscure data in hopes of discerning future trends? If you failed to answer yes to any of these questions, then market timing may not be for you. The belief that you, or any particularly person, can foresee the direction of the stock market is a seductive one. Some investors are confident that, with proper research, they can make money by snapping up equities when prices are low, and shifting their investments into cash or bonds when the market hits its peak. But longitudinal studies have shown that most market timers not only fail to beat the market, they may actually earn less over time than buy-and hold investors. However, many armchair investors persist in the belief that, by carefully following business news and trusting their “gut” instincts, they will be able to out-smart the market. Some study the stock tips in personal finance magazines, others hope to glean additional insight from analysts’ reports and specialized investment newsletters, and still others attempt to mine all the available data, crafting complex simulations of how the market is likely to behave in the future. But if financial professionals who do this for a living struggle to accurately predict where the stock or bond market might go, private investors are even less likely to outfox the markets. As soon as a piece of business or economic news hits the airwaves and the Internet, analysts and brokers react immediately to the information (this is call "The Efficient Market Theory" in finance). Because of financial professionals acting quickly, the market mechanics create a situation where the stock market almost always reflects all the known information at any given moment in time. And even if an individual investor were able to develop an analytic model with some real predictive value, unexpected events—such as a terrorist attack, a natural disaster, or even a political scandal—typically leads to sudden and dramatic market fluctuations that no model based on historical data could have anticipated. It is only natural that investors would want to find some way to sit out bear markets and get back just in time for the next bull run. It is useful to keep in mind, however, that even the slowest equity markets have some bright spots. A well-diversified portfolio will help you protect against loss and capture whatever gains might occur in a market downturn. Investors run a big risk by selling when they believe stocks have reached their peak. They may turn a profit when cashing in their equity holdings, but they could also miss out on some of the market’s best cycles. Being absent from the market for only a few of the days or weeks with the highest percentage gains can decimate a portfolio’s returns over time. Market timers who sell frequently also lose money to transaction costs and taxes, and miss out to a large extent on the compounding effect that benefits investors who remain in the market consistently. The vast majority of investors are better off, instead of trying to time the market, just being in the market. Of course, investors need to be in the right investments that match their risk tolerance and time horizon. Trying to pinpoint the right time to invest in the stock market is an exercise in futility. If you have a longer period to save, owning equities provides the most effective hedge against inflation and taxation available. Since it is impossible to know where the market might go from here, remember, that long-term investment success is achieved not by timing the market, but by time in the market. -Paul R. Rossi, CFA  Television and radio business news reports lead with it almost daily. Serious financial discussions begin with it. Many economic discussions are often centered on it. The “it,” is the “Dow,” or more accurately, the Dow Jones Industrial Average, and it remains the most widely used measure of stock market performance by many main street pundits. So what exactly is the Dow Jones Industrial Average? The Dow is a price weighted “average” of some of the largest and well-known companies in the United States. But how the Dow is measured, its history, and current holdings are typically not so well-known. Let's take a brief look at market history, how the Dow has changed over time, and what the current companies that make up the Dow. Charles Henry Dow first devised his market “average” in 1884. The first “Dow” average consisted of 11 stocks, nine of which were railroads--the large growth companies of that era. Not surprisingly, not one railroad company remains in the index today. The Wall Street Journal first published the Dow in 1896, covering an average of 12 stocks. During the period from 1916 to 1928, the Dow average increased to 20 stocks and then in 1928, the now familiar 30-stock Industrial Average was born. All of the original names have disappeared after GE's removal in 2018; they have either merged, changed their name, been removed from the index, or gone out of business. If we were to use an example Dow of 28,000, it would mean that the average share price of the 30 Dow stocks is $28,000, and, of course, no Dow stock sells for anything close to that level. How then, do we make sense of this “average”? Here’s how it works. The Dow average is constantly adjusted for stock splits, stock dividends, and changes in market valuations of the component stocks. As an example, when a stock splits, the share price decreases and the number of shares increases proportionally, with total value to the shareholder unchanged. For example, a stock selling for $50 per share splits two-for-one. If you owned 100 shares, you now own 200 shares worth $25 per share. Overall, nothing has changed in terms of value. You’re probably now seeing that this function is going to impact the average price because even though the price of the shares came down the value of the company remained unchanged. So, this is what creates some complexity. While the impact of stock splits on individual investor holdings is straight forward, such changes in share price have an impact on the Dow. Consider the hypothetical Dow “average” of 28,000, and, on the same day, all of the stocks split two-for-one. If no adjustments were made to allow for the split, the Dow would “drop” to 14,000 overnight without any change in the underlying value. In order to compensate for these price changes which produce no effective change in total value, the Dow average is constantly adjusted by altering the “divisor” in the pricing formula. The divisor is simply that number when divided into the total share prices of the 30 component stocks, creates an equivalent basis on which to compare a current reading with any other historical reading since 1928. Each time a split occurs, the divisor must be adjusted downward; if this did not happen, the average share price of a Dow component stock (based on a Dow of 28,000) would really be $28,000. When the 30-stock Dow average was created in 1928, the divisor was 16.67. This number was derived to establish a price relationship to earlier averages so that historical comparisons would be meaningful. Over the years, the divisor has declined steadily, falling below 1.0 in 1986, at which time it effectively became a multiplier. (A quick review of the math will show the result of dividing a number by a number less than 1.0 becomes a larger number—that is, a divisor less than 1.0 effectively becomes a multiplier). The current multiplier is 0.152. So a $1 price move in any Dow component translates to a swing of 6.58 points to the Dow. While many financial professionals use other broader measures of market activity such as Standard & Poor’s 500 Index (the S&P 500) or the Russell 2000, the Dow is still considered a reflection of the overall stock market is a testimony to how powerfully ingrained the Dow is to our collective thoughts. Below is the current list of what makes up the Dow Jones Industrial Average, along with recent market values for each company along with their respective 5-year total return.  -Paul R. Rossi, CFA |