I'm thankful for so many things in my life, that sometimes I feel I've won the lottery. Why do I say this? Because it's true. First, let's start with family: I have a great relationship with my wife and children that I feel very fortunate. I'll admit, I'm very intentional in how I communicate and interact with my family and don't take it for granted. While 2020 has been an extremely challenging year for so many people, I feel very fortunate because it's allowed some very positive things to come out of an extremely challenging period - and I believe many times challenging situations can provide positive growth, sometimes in truly unexpected ways. Second, my clients and friends: I never take for granted the relationships outside of my family. I have a special relationship in my clients lives as I learn what's most important to them and I get to help them achieve it. There is tremendous amount of trust that my clients must have in me, and I don't take this for granted. In addition to my clients, I have great friends that I truly appreciate. Many of these friendships span more than 25+ years with countless memorable memories. So in the spirit of Thanksgiving and being thankful, I am thankful for and would like to say thank you to my:

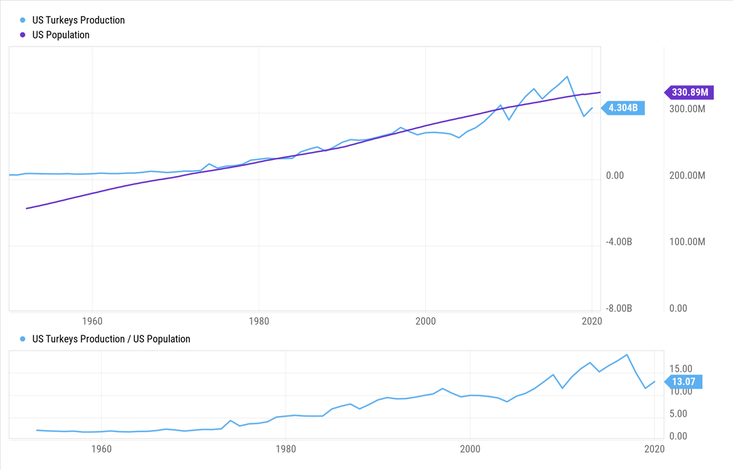

And this blog wouldn't be complete without a Turkey chart or two. Enjoy!  Turkey Production is out pacing US population growth! Is there an investment opportunity here? :)

-Paul R. Rossi, CFA

0 Comments

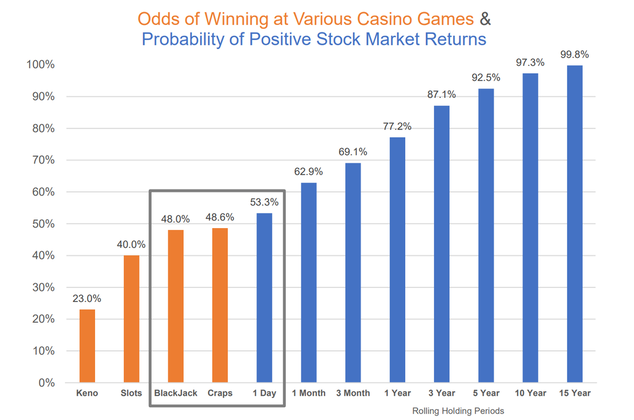

I've heard many people over the years express their concern that investing in the stock market feels like gambling - where there is little chance of winning. The remark typically sounds something like this, “The market goes up and then it goes down and you don't make money, it feels like gambling.” So I decided to see if there is some validity to this belief. First I looked at various casino games and the odds of winning. Then I gathered stock market data from 1937 through September of 2020, using rolling periods to provide as many measurement periods as possible. Keep in mind, during this 83-year time period the market experienced 14 recessions (including our current recession) , 2 world wars, the Cuban missile crisis, the assassination of JFK, the crash of 1987, 9/11, Covid, and countless other tragic events that rocked our world. Interesting enough, after combing through the data, I can understand how people might feel this way, because over the very very short-term the stock market has had similar chances of generating positive returns as some casino games. Take a look at the chart below: Black Jack, Craps, and the 1-Day holding period for the stock market have similar probabilities of winning (historically). What also might be enlightening is the probability of "winning" in the stock market dramatically increases as the holding period increases. Over the last 83 years, the probability jumps to over 92% if an investor held for 5-years and is over 99% with a 15-year holding period. Imagine if you could play casino games and have percentages approaching anywhere near these levels. Maybe the moral of the story is what we all try to teach our children, that patience truly is a virtue.  I like the long-term odds of winning in the stock market. As the Worlds Most Interesting Man might say, “Stay patient my friend.” -Paul R. Rossi, CFA  Investors with complex needs are increasingly seeking out independent advice—and one way to ensure you’re getting independent advice is to work with an independent financial advisor. Sounds pretty straight forward, if you want independent advice, then seek out firms that are independent. So what are 5 benefits of working with an independent financial advisor?

-Paul R. Rossi, CFA  In the short-term the markets trade on greed and fear, but in the medium to long-term, they trade on First Principles.

What are First Principles? Before we get to that, let us understand what greed and fear are as it relates to investing. Greed is the idea of not wanting to lose out on an opportunity to make money especially when you see others around you making what seems like easy money. As Warren Buffett said, “Long ago Sir Isaac Newton gave us three laws of motion which were the work of genius, but Sir Isaac Newton's talents didn't extend to investing: He lost a bundle in the South Sea Bubble explaining later, ‘I can calculate the movement of the stars but not the madness of men.’ If he had not been traumatized by this loss Sir Isaac might well have gone on to discover the 4th law of motion for investors as-a-whole returns decrease as motion increases.” Sir Isaac lost millions in today’s dollar equivalent by falling into the greed trap by seeing others around him making seemingly easy money on what amounted to nothing more than a house-of-cards. It didn’t end well for him. Greed is dangerous. On the other side of greed is fear. “Fear is an emotion induced by perceived danger or threat, which causes physiological changes and ultimately behavioral changes, such as fleeing, hiding, or freezing from perceived traumatic events. Fear in human beings may occur in response to a certain stimulus occurring in the present, or in anticipation or expectation of a future threat perceived as a risk to oneself. The fear response arises from the perception of danger leading to confrontation with or escape from/avoiding the threat, which in extreme cases of fear can be a freeze response or paralysis.” – Google search and definition. Interestingly enough, fear like greed can be immeasurably harmful. This can happen by taking action when doing nothing is the right thing or conversely by freezing-up and not taking action when you should. Fundamentally this comes down to rationality. The more rational you can become, the more successful as an investor you can become. How do we reduce our level of fear and strive to be more rational? By taking a step back from the situation and thinking about what’s happening and asking ourselves a series of questions.

While there are many more questions that can and should be asked prior to determining what the right course of action is, you can see that self-reflection and having a deeper understanding of the situation is paramount during times of heightened uncertainly. What is critically important is getting to a deeper understanding of the situation, what is called getting to the “First Principles”. What are First Principles? First Principles thinking is a process by which a person seeks to break down a problem to its simplest elements to find a solution. The first-principles approach has deep roots, in fact, it was a process credited to Aristotle. Over 2300 years ago, Aristotle said that a first principle is the ‘first basis from which a thing is known’ and that pursuing First Principles is the key to doing any sort of systemic inquiry. Quite simply, First Principles is the most fundamental idea which makes it the highest in importance when trying to understand a particular subject. So, what are First Principles in terms of investing? First Principles idea in investing is the understanding of ‘valuation’ and how to value an asset. Ironically, the concept is quite simple: The value of any income producing asset is the present value of its future cash flows. What does this mean? It means taking all the projected future cash flows that a company will generate in the future and discounting these cash flows to the present value using an appropriate discount rate. When you do the math, you find that the vast majority of a company’s value is wrapped up in the future years’ cash flow and not in this year or even next years’ cash flow. Click here to see an example. Investing First Principles: A company’s intrinsic value is based on its long-term cash flows that will be generated far into the future. Greed and fear will always be a part of the market. Volatility isn’t going away. What’s most important is understanding the First Principles approach to the market and realizing that individual companies and subsequently stock markets are valued on their long-term cash flow generating ability. Everything else is greed and fear. -Paul R. Rossi, CFA  Annual rebalancing can help boost returns and reduce your volatility. As 2020 wraps up, it’s time for investors to start thinking about rebalancing their portfolio(s). And while it is important to examine rebalancing every year, it can be especially important this year due to the large return differences in asset classes. For example, through early November 2020, looking at the variability of returns from different sectors and market indices is quite dramatic:

Rebalancing Matters Rebalancing is the process of buying and selling assets to move your portfolio in alignment with its original target allocation. Restoring your mix can both boost returns and lower volatility, unfortunately many investors do not understand why and how to properly execute this process. Without understanding the science of rebalancing, which is the theory behind it, average investors do not properly implement the art of rebalancing their portfolios, the actual shifting of the right assets. At best, they simply buy and hold their investments. A Basic Example of Rebalancing As a simple example, imagine two investments, A and B, which on alternate years have returns of 0% and 30% respectively. Investment A has a 30% return on odd years while B has a 30% return on even years. Over any two-year period, buying and holding either A or B will result in a 30% investment gain. At first glance, most investors would think that, in this scenario, you could not do any better than a 30% return over the two years. But an asset allocation of half in investment A and half in investment B has a total return of 32.25% for the two years. The extra 2.25% return comes from rebalancing. The portfolio had a 15% return during the first year and then is rebalanced. Half of the profits from investment A are sold and put into investment B, where they appreciate the next year and receive a compounded return. This is an example of rebalancing both reducing the volatility and boosting returns. In this example rebalancing smooths the returns to a consistent 15% each year and compounded returns adding a 2.25% bonus. Unless You Can Predict Markets Yes, it would be wonderful to invest everything in A the first year and everything in B the second year. If you had the precognition to do this, you’d earn 69%. But this type of return foresight is next to impossible. We are much more likely to chase returns than anticipate them. The worst scenario of this is investing everything in investment B the first year. Then, enticed by the returns of investment A, selling B and investing everything in A the next year. In our example, this strategy of chasing returns results in no return at all. This strategy is sadly common because people wrongly believe that an investment will continue to go up just because it went up in the past. Although some people talk about “the momentum of the markets,” the stock markets are much more complex and volatile than such simplistic strategies. The rebalancing bonus becomes clear when looking at many decades of historical data. For any one decade, one investment choice randomly has better returns and, with perfect hindsight, it appears that you should have put everything in that winner. But none of us has precognition. Instead, investing in non-correlated asset categories and then rebalancing to that asset allocation has the best chance of seeing the gains of one asset class compound in a different class the next year. There is a complex formula to compute the bonus produced by the discipline of regularly rebalancing your portfolio. The bonus is increased when the correlation between the two investments is low and the volatility of each of the assets is high, as in our simple example. The Rebalancing Bonus Consider three investments which each year have annual returns of -16%, 7%, and 30%, but rotate which year each investment has each return. If you invest equally in each and rebalance every year, you receive an average return of 7%. But if you start invested equally and don’t rebalance, your return drops to 5.33%. This is because if you don’t rebalance after a fund grows by 30%, then more money will show the -16% return in subsequent years. In the same way, not rebalancing the money that has a 16% drop means that less money receives the upcoming 30% return. When an asset class has just dropped significantly, it is difficult to sell some of the best performing class and buy more of your worst performing category. However, the greater the difference between asset class returns, the higher the rebalancing bonus. Rebalancing & Volatility The markets are inherently volatile. They experience what is called “lumpy tails,” which means there are more returns outside of the normal bell curve. The stock market’s normal volatility (about 18% standard deviation) suggests a rebalancing bonus of about 1.6%. What’s interesting, if the market were more stable, the rebalancing bonus would drop. At a 5% standard deviation for example, the bonus might only be 0.12%. This is why rebalancing only bonds does not have as much of a rebalancing bonus. The normal volatility of the bond market is only 6.9% (standard deviation), which suggests a rebalancing bonus of 0.28%. Rebalancing from stocks into bonds may reduce your returns on average since bonds have a lower average return. There are several articles suggesting that rebalancing does not boost returns, but these are about rebalancing out of stocks and into bonds. Moving into bonds may be a part of rebalancing, but the goal of such movement is not to boost returns. Bond allocations are useful to support portfolio withdrawals and limit risk. Rebalancing can increase returns because market volatility makes it difficult, if not impossible, to predict which asset class will perform well in the future. The asset that recently went down may be the next to go up, while the last to go up may be the next to go down. Thus, systematically rebalancing back to your asset allocation gives you the best chance of compounding and therefore boosting returns. As always, an important aspect to investing is knowing what you own and why. |