We recently celebrated Labor Day and it’s a good time to reflect on why we work and what we derive from it. The ideal answer should be that it gives your life energy and meaning. If it doesn’t, you might want to consider how to move in that direction. Labor Day became a federal holiday in 1894 and now also marks the unofficial end of summer. Summer trips wind down, students leave for college, football season gears up and we anticipate the cooler days of fall with enthusiasm. This is especially true if you are in a hot area of the country, and who doesn’t appreciate a 3-day weekend? Work Matters There is now a common understanding that meaningful work is a major component of human well-being. Interestingly, it does not matter whether the work is paid, volunteer or pro- bono, or you are working hard at home raising children. What We Do Matters Researchers at the Gallup organization have been exploring the subject for decades. A not-so-startling finding: Our happiness and feelings of well-being are a function of liking what we do each day. Tom Rath and Jim Harter explain in their book, Well Being: The Five Essential Elements, “…at a fundamental level, we all need something to do, and ideally something to look forward to, when we wake up each day. What you spend your day doing each day shapes your identity, whether you are a student, parent, volunteer, or retiree…” Yet only 20% gave a strong “yes” when Gallup researchers asked, “Do you like what you do each day?” If 80% are unhappy with daily activities, the rest of their life is likely to be out of whack and it’s likely your well-being will suffer. Well-Being Matters If you are to successfully live your life, your health, relationships, social connections, your sense of place, the fact that you are where you belong in terms of where you live, work, and interact with friends and people, as well as your spiritual home, are all key components of well-being. Defining Strength When you reinforce your talent with knowledge and skill, you have strength. A talent is a naturally recurring pattern of thought, feeling or behavior productively applied. A skill is the ability to move through the fundamental steps of a task. Knowledge is what we know. A strength, then, is a powerful, productive combination of talent, skill, and knowledge. When you are doing anything from strength, you feel it, you know it, and you love it. If you want to recalibrate and infuse your life with new energy, a revitalized sense of purpose, and a sense of comprehensive well-being, remember that: What you do matters. You matter. Build your strengths. -Paul R. Rossi, CFA Picture: SR-71 spy plane, it was the United States most advanced and fastest flying plane in the world, literally flying faster than a speeding bullet. It carried no weapons and was designed in an era when engineers used a slide rule. The SR-71's sole purpose was to keep the United States safe by being able to capture photos of our enemies' movements. The SR-71 was shot at many times, but was never shot down, as it was designed and flown by people who had an unbelievable sense of purpose.

0 Comments

What is asset allocation? “Don't put all your eggs in one basket,” this phrase probably says it most succinctly. How important is Asset Allocation? Studies have shown that asset allocation decisions can explain more than 90% of the variation in a portfolio's return over time. Asset allocation involves diversifying and owning various asset classes. These asset classes might include domestic stocks, bonds, international equities, real estate, cash, and several other categories. Ideally, the various asset classes do not move in tandem (highly correlated) with each other. As a group, every asset class carries a unique expected rate of return and level of risk. Typically, the assets will react differently under varying market conditions, such as during a strong economy, slow growing economy, shrinking economy, low inflation, high inflation, etc. As an example, one asset class may rise in value while another asset class falls over the same period of time. The ultimate goal of asset allocation is to construct a diversified portfolio that pursues the maximum rate of return in exchange for taking on a certain level of risk. One way to measure this return to risk proportion is called the Sharpe Ratio, named after Noble prize winner William F. Sharpe. The Sharpe Ratio = (return of the portfolio - return of the risk-free rate) / (standard deviation of returns). The idea is to generate the highest returns for a given unit of risk, i.e., the higher the Sharpe Ratio the better. Some research has shown that portfolios invested in assets that are not highly correlated with one another may perform better over long-time horizons and carry less risk than portfolios that are heavily weighted toward one type of investment. We might call this, getting a "free lunch"...stronger returns with less risk. These well diversified portfolios are sometimes referred to as efficient portfolios. Efficient portfolios are designed to pursue the maximum rate of return in exchange for a given level of risk. What are some ways to go about implementing an asset allocation plan? Strategic Strategic this method establishes and then maintains a specific combination of assets based upon expected rates of return for each asset class. Tactical Investors actively overweight and underweight segments of the market to capitalize on potential short- term market opportunities. When investors reached their short-term profit goals or do not have a strong opinion on segments and sectors they may buy or sell positions in order to return to a core asset allocation Valuation Based with this approach, investors constantly adjust the mix of assets based on their (relative or absolute) valuation. As certain investments get cheaper, and investor will buy more of the asset class and sell as they get more expense. For example, investors may sell existing positions in asset classes that have increased in value in and buy assets that have decreased bringing the mix back to the long-term proportions that are best for the investors risk and return goals. Rebalancing & Flexibility The importance of establishing the right asset allocation mix is important, however maintaining it overtime is equally important. Over time as the different assets move up and down it may become necessary to make adjustments to maintain the right proportion. This adjustment process is called rebalancing. Although it is important to create an asset allocation plan when constructing a new portfolio, it is equally important to assess your allocation over time and remain flexible. Investors can add new investments to fill gaps in their target allocation or to adjust their portfolios as their life situation and goals change. An annual or quarterly review of your asset allocation plan also gives you an opportunity to review other aspects of their financial plan (risk tolerance, goals, major life changes, etc.). Your asset allocation should support and sync with your overall financial plan. It is important to understand your portfolio's asset allocation, as it may be the single most important determinate of your portfolio's performance. -Paul R. Rossi, CFA Bipolar disorder is a mental disorder that causes unusual shifts in mood, energy, and activity levels. These moods range from periods of extremely “up,” elated, irritable, or energized behavior (known as manic episodes) to very “down,” sad, indifferent, or hopelessness during the depression phase. – National Institute of Mental Health (NIH). I’m not a mental health expert (my wife is), but doesn’t bipolar disorder sound eerily like what the stock market suffers from? The stock market goes through wild swings of optimism and then can quickly shift to periods of severe depression, then back to optimism, with this cycle continually repeating. Want just a few examples?

Going back a bit further we can see similar patterns throughout the stock markets history.

If we deem that the stock market suffers from bipolar disorder. What can we do about it?

Maybe we can learn from what the National Institute of Mental Health recommends for treating bipolar disorder in individuals. First, we need to understand it's a lifelong illness and usually requires lifelong treatment. However, the NIH says following a prescribed treatment plan can help people manage their symptoms and improve their quality of life. Their (abbreviated) treatment plan includes a combination of:

Let's use the NIH as a template for our suffering stock market and related investors. First, we need to understand that the stock market suffers from this condition and it's lifelong.

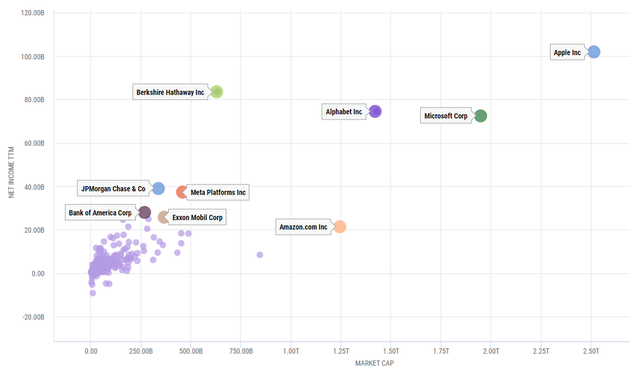

As investors, we will be dealing with the stock market and its bipolar disorder for the foreseeable future. Since we as individuals can’t “fix” the disorder the stock market suffers from, we need to decide how we are going to interact with the market when it’s going through its various periods of hopelessness and manias. -Paul R. Rossi, CFA Why are so many of the same companies mentioned in the news day in and day out? The Scatterplot below might help explain why: The chart shows all 500 companies of the S&P 500 represented by light purple circles. In contrast, some of the largest companies are displayed in other colors. These highlighted companies each earned (Net Income) $20+ Billion dollars over the last 12-months and several are worth over a Trillion dollars.

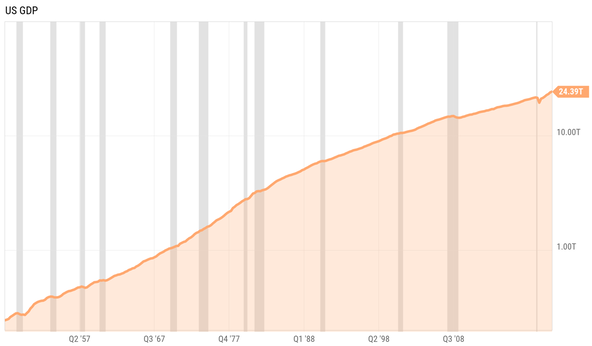

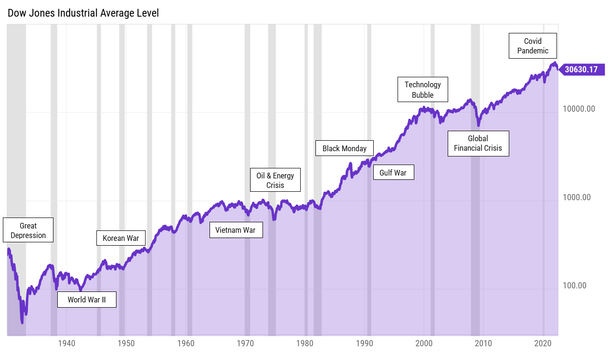

And now you know why these companies are so prominently featured in the news. They are behemoths in every sense of the meaning. When they hire or fire, enter new markets, create new products, build new buildings, they have a deep and wide impact within their respective industry. -Paul R. Rossi, CFA  Above is a chart of the U.S. GDP (Gross Domestic Product from 1947 - 2022). Since the end of World War II, the U.S. economy has grown tremendously. GDP is now a staggering 10 times larger than it was back in 1947. Oh, and by way, this includes enduring 12 recessions (grey lines) along the way.  Above is a price chart of the Dow Jones Industrial Average going back to 1930. It includes some major world events, The Great Depression, several wars, and 15 recessions. If I was a betting man (and I am), I wouldn't bet against the United States continuing to grow and do well over time. The key part of this phrase being, "well over time." We are going to experience some tough times both now, and in the future...this unfortunately is unavoidable. Plan accordingly. Tough times don't last, but tough people (and investors) do. -Paul R. Rossi, CFA

Many times opportunity comes wrapped inside a scary situation, dealing with hardship, or simply accepting change. But nearly every time it ends up requiring a person to step outside themselves and take the proverbial leap of faith. What’s a Bear Market? It’s an opportunity… and it’s scary, it's a hardship, and it requires taking a leap of faith. What is the conventional definition of a Bear Market? The Securities and Exchange Commission (SEC) defines a Bear Market as a period of at least two months when a broad market falls by 20% or more. The Standard & Poor’s 500 index, which includes virtually all of the largest and most well-known U.S. companies is in an “official” bear market (if you didn’t know this already), since its peak on Jan. 3, 2022. Since 1928 there have been 26 Bear Markets with an average length of 289 days. No doubt about it, psychologically a Bear Market can be challenging. The impact can be particularly hard for investors who do not have a well-designed plan as they see their retirement accounts and investment portfolios shrink. And this can create a self-fulfilling cycle, as investors perceive an impending bear market tend to prompt investors to sell even more, thus pushing prices down further and prolonging the pain. What psychologists call a “Negative Loop Cycle.” What's the good news and what opportunity might a Bear Market provide? For those investors who have psychology and time on their side, a Bear Market can offer:

So during a Bear Market, there are quite a few things an investor might do, and probably the most important idea you might consider changing is the nomenclature from Bear Market to “Opportunity Market.” -Paul R. Rossi, CFA  Let’s break down the metrics and details used that every person who invests in their company’s retirement should pay attention to.

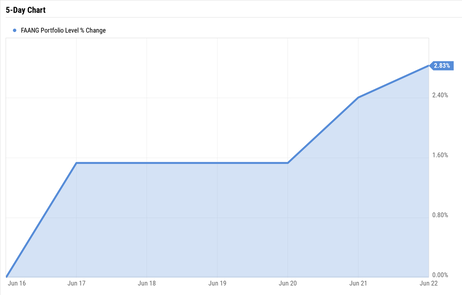

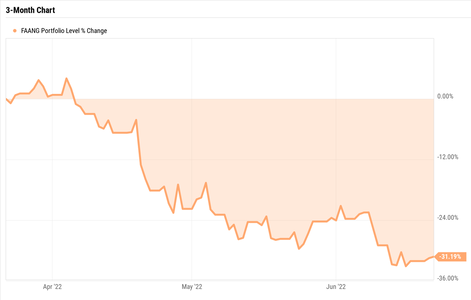

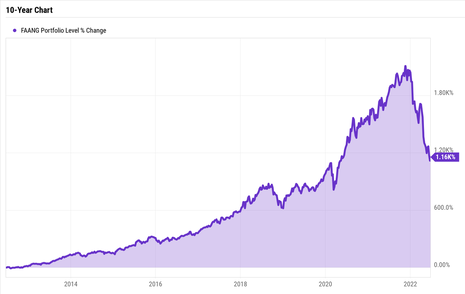

By identifying and understanding these metrics for evaluating funds, you are one step closer to finding the best funds to invest in to help you reach your financial goals. -Paul R. Rossi, CFA For a lot of investors, when you bring up the term "FAANG," they understand what you are referring to, as the term has become quite ubiquitous. The term FAANG refers to the stocks of: Facebook (Meta) Apple Amazon Netflix It can be argued that these five companies have changed the way we work, live, and communicate. They have changed our lives in so many ways...and along the way investors have done quite well (mostly). But like most things, it depends how we measure returns, or more accurately how long has an investor has owned these companies. Investors get dramatically different answers to the question, "How well are these companies doing?" depending on the time period they are measuring. Let's review how well they've done over the following time periods:

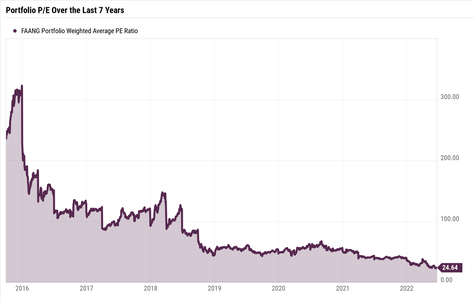

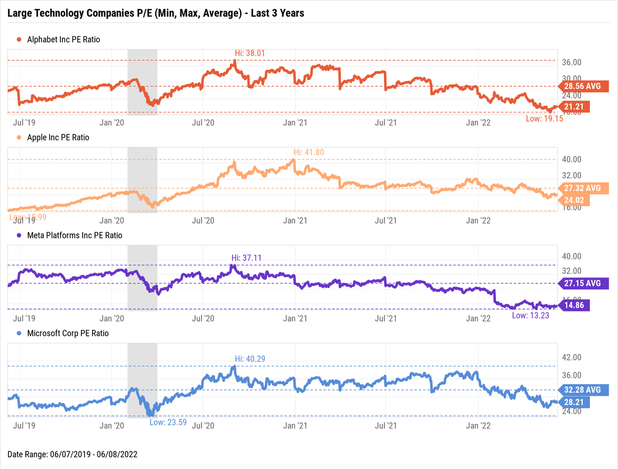

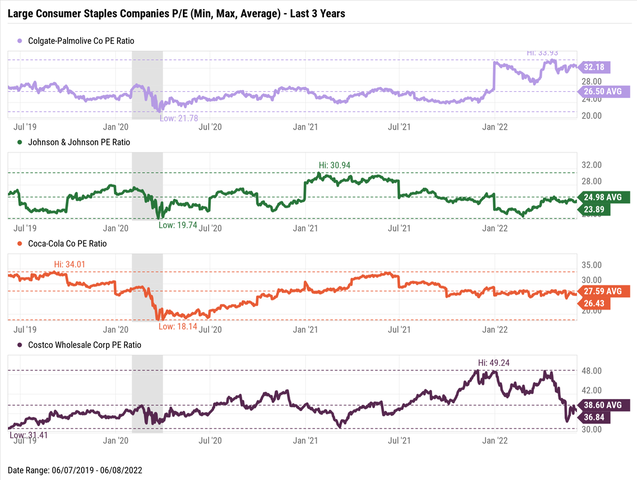

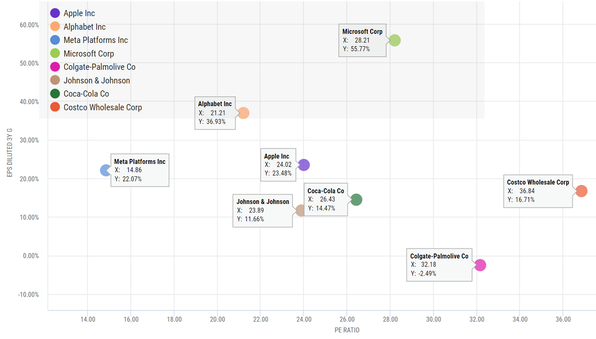

Short answer is, they are Up, Down, Down, Up, Up, and Way Up.  5-Day Return: UP  3-Month Return: DOWN  1-Year Return: DOWN  3-Year Return: UP  5-Year Return: UP  10-Year Return: WAY UP Investors have been handsomely compensated over the last 10-years, gaining more than 10x their original investment. And during the last several years the P/E Ratio (a valuation metric) has been coming down on these companies collectively (chart below). This is good news for investors. New investors are now able to buy these companies at valuation levels never seen before.  What's interesting is that many other companies and their corresponding stock have similar patterns, over the short-term they tend to be up and down quite a bit. The next time you hear the old adage, "What goes up, must come down." You can ask them, "Over what time period?" -Paul R. Rossi, CFA Financial professionals rely on long-term historical averages when making capital market assumptions and not all starting points are the same. Investors should take current stock valuations into account as they make financial plans and allocate assets. Getting into the market when stocks are highly valued can work against an investor. Even over time horizons as long as 20 years or more investing in high valuation environments can lead to below average returns. Conversely if stock valuations are low when the investor begins, this can lead to above average returns over an economic cycle. Even young investors with long time horizons should be mindful not to assume too much risk in an overvalued market even if the long-term return eventually averages out to what was initially anticipated. Lets take a look at an interesting situation between historical growth rates and a well-known valuation metric used by financial professionals called the P/E ratio. The ubiquitous P/E ratio, which is defined as the (Price per share) / (Earnings per share). The P/E ratio has units of years, which can be interpreted as the number of years of earnings to pay back purchase price. P/E ratio is often referred to as the "multiple" because it demonstrates how much an investor is willing to pay for one dollar of earnings. Right now, large well-known Technology companies are being priced at valuations below their historical 3-year average (chart below).  Now let's compare this with four companies below which are classified as "Consumer Staple" companies. These are companies that sell essential products used by consumers. These are typically goods that people are unable or unwilling to cut out of their budgets regardless of their financial situation. This makes these companies non-cyclical in nature.  Below is a Scatter Plot of both the Technology and Consumer Staple companies from above. This graph is comparing their current valuation (P/E on the x-axis) vs. 3-year Earnings per Share Growth (Y-axis). As is apparent, the Technology companies have had substantially higher earnings per share growth (Y-axis) while their current valuations (X-axis) is lower. On the Scatter Plot, the upper left corner would be the best quadrant and the lower right would be the worst quadrant.  So what are these numbers and charts saying? These 3 charts are conveying the following:

What does all this mean? Collectively the four Technology companies look inexpensive relative to the four "so called" safer Consumer Staple companies. Keep in mind this doesn't mean that these Technology companies can't go lower. All else being equal, it's better to own a company or a collection of companies with higher earnings growth and a lower valuation. -Paul R. Rossi, CFA

Seven seconds. Seven seconds is the somewhat popular belief of a goldfish’s memory. Apparently after seven seconds the goldfish has completely forgotten what happened prior. Whether this is true or not, let’s go with it for now. I would say in some sense, having a goldfish's memory can be an advantage. However, understand that the media wants you to have a long memory, more akin to the memory of an elephant (assuming you believe that elephants have great memories). They want to fill your head will all the things that went wrong, are currently going wrong, might go wrong, and will go wrong far into the future after we have all passed away (recent news title: the sun will die in approximately 5 billion years and how this will impact us). Why? It keeps us all hooked to what they are going to say next. And that’s how they make money. Never forget that. The financial media would like you to believe that it's important to know what happens every day in the markets. They want you to know when the market is down 3% for the day, down 5% for the week, or down 10% for the month. In this case, be like a goldfish. Give it seven seconds, no more. I don't know anyone that measures their own personal success in days, weeks or even over the course of a year. For example, college typically takes four years or more for an undergraduate degree and a graduate degree can take several more years after that. We all measure the graduate on their success in graduating after years of studying. Professional success is no different. It takes years to become an expert. I’d like to hear of any professional athlete who mastered their sport in a day, week, month, or even a year. How about a surgeon? How many years before they are considered an expert in their field? Physicist, Contractor, Accountant, you name it, no one masters anything measured in anything smaller than years or decades. Investing success is no different, it is measured in years and decades, not in days, weeks, or months. Mastering the markets is more about mastering yourself rather than actually mastering the markets. How do you master yourself? By mastering your emotions and your memory. This is what makes investing so hard. -Paul R. Rossi, CFA  What does Warren Buffett Say to Hedge Against Inflation? Before we get his answer, he says this about inflation…it hurts almost everybody, it hurts stock, bond, and cash-under-the-mattress investors. Warren Buffett is chairman of Berkshire Hathaway and the most successful investor of all time. How successful has he been? He has built his quasi vestment holding company Berkshire Hathaway into the 7th largest company (measured by market cap) in the United States. Over the years, Buffett has done this by acquiring entire companies and folding them into Berkshire Hathaway, some of these include such names as See’s Candy, GEICO insurance, Burlington Northern Santa Fe railroad, General Re Insurance, and dozens of other companies. In addition to this, Buffett also buys stock in public companies, currently his 10 largest stock holdings are:

In terms of inflation, he’s recently said, “It’s extraordinary how much [inflation] we’ve seen,” as he talked about soaring prices at his Nebraska Furniture Mart and many other Berkshire subsidiaries. “Inflation swindles almost everybody,” Buffett said. Probably one of the most important things that he has recently, the very best defense against inflation is to be great at what you do, producing a great product/service that is in demand and offering a product/service that people will pay for. Specifically, he said: “The best protection against inflation is your own personal earning power…No one can take your talent away from you,” Buffett said. “If you do something valuable and good for society, it doesn’t matter what the U.S. dollar does.” When asked to predict inflation, Buffett said that predicting future inflation is a fool’s game, and that no matter what someone might suggest, the truth is that no one can really know how much inflation there will be over the next 10 years, or for that matter in the coming year. -Paul R. Rossi, CFA  You never know what you are going to get. Most of us understand what a 1% chance of a flood happening over a 1-year period means. We recognize it’s highly unlikely to happen. Our understanding can become a bit murkier when we add additional variables and years to the situation. For example: What are the chances of this same flood happening over a 100-year period? The likely hood goes up quite a bit, it’s more likely than not (63.4%) that there will be a flood within the next 100-years, even though the 1-year probability is just 1%. As investors, macro events can have a direct and dramatic impact on our portfolio. We need to understand that “bad” things can and do happen. Let’s start with a very short list of some possible “bad” events:

If we put just a 1% on each of these independent events happening in any given year, over a person’s lifetime, say 80 years, there is a near certain probability (95.9%) of any one of these bad events happening. Now imagine if we add just a few more possible events to this list: global recessions, social unrest, minor wars, assassinations, inflation, etc., you can see where this is going…bad sh*t happens. The future is uncertain and we should assume a lot of “bad” stuff is going to happen, so it’s important to accept this fact. The fact that we are never going to know what we are going to get. I would add, that even with all the “bad” stuff that will happen in the future, more “good” stuff will actually happen, just look at how far we have come from our cave dwelling days. As Warren Buffett has said more than once, “Our best days lie ahead.” Most of us would agree that a carefully constructed investment portfolio can weather a lot of bad economic storms, none can withstand the fatal blow of an investor who panics sells or who invests in things they don’t understand. I like the idea from Morgan Housel, a partner at a VC firm that said, “Save like a pessimist, invest like an optimist.” -Paul R. Rossi, CFA  Cash Flow Questions

Asset and Debt Questions

Tax Planning Questions

Long Term Planning Questions

When outside factors like the economy change, or might change, it’s a good idea to review your financial situation to determine if adjustments might be warranted. -Paul R. Rossi, CFA  Donald Rumsfeld served as the Secretary of Defense under two different Presidents. During his second stint in 2001, he wrote a memo to the President, “I ran across this piece on the difficulty of predicting the future, written by one of the folks here at the Pentagon, Lin Wells. I thought you might find it interesting.”

This was written and sent to the President 5 months prior 9/11/2001. -Paul R. Rossi, CFA  Once upon a time there was a Chinese farmer whose horse ran away. That evening, all of his neighbors came around to commiserate. They said, “We are so sorry to hear that your horse has run away. This is most unfortunate.” The farmer said, “Maybe.” The next day the horse came back bringing seven wild horses with it, and in the evening, everybody came back and said, “Oh, isn’t that great fortune, you now have eight horses! What a great turn of events.” The farmer again said, “Maybe.” The following day, the farmer's son was riding one of new horses to try to break the horse, he was thrown and broke his leg. The neighbors then said, “Oh isn't that horrible?” And the farmer responded, “Maybe.” The next day the conscription officers came around to draft young men into the army, and they rejected his son because he had a broken leg. Again, all the neighbors came around and said, “Isn’t that great!” Again, he said, “Maybe.” "The whole process of nature is an integrated process of immense complexity, and it’s really impossible to tell whether anything that happens in it is good or bad, because you never know what will be the consequence of the misfortune; or, you never know what will be the consequences of seemingly good fortune." - Alan Watts Investing can feel like a roller coaster, with so many ups and downs it can be hard to understand if what is currently happening is actually good or bad. -Paul R. Rossi, CFA  A few pointers to help ensure you don’t endure a double-drubbing this time. Stoicism amid market turmoil is tested hard when a tsunami of grim investment headlines and plunging stock prices hit the market. It is Déjà vu All Over Again? Let’s look at recent history. In 2008, the problem was

This time the causes are different, but the current conditions are very similar, investors worried about

As we've all come to understand, history doesn't necessarily repeat itself, but it often rhymes. The effect remains the same: a double-digit drop in stock prices. Currently the S&P 500 is down over 12% and the technology heavy NASDAQ is down over 20% (official bear market territory). Consider the mistake some investors made exiting markets in 2008-09. Or those exiting markets in March of 2020. Those investors selling locked in steep losses and often were too nervous to get back into markets as prices rebounded. The result: a double-drubbing. Here are some pointers to keep in mind in the current market turmoil. Stocks Outperform Other Asset Classes Even considering periods of steep decline. Investing in stocks means remaining disciplined through both good times and bad – and no formula exists for consistently timing markets to buy at the bottom and sell at the top. Investors who attempt such timing often get sub-par returns because they actually often end up doing the opposite: buying high and selling low. As Warren Buffett has said, “Be greedy when others are fearful, and be fearful with others are greedy.” Higher Historic Returns on Stocks Go Hand in Hand with Higher Volatility Stock investors have been compensated historically for enduring higher volatility. Conversely, we expect a lower return from bonds in exchange for lower volatility. Pursuing higher long-term returns means accepting accompanying risk, period. Your portfolios should be based on your unique financial and personal circumstances. This conceptual purpose doesn’t change if stocks correct 10% or rise 10%. Yes, you should rebalance regularly. But don’t buy or sell in a panic. If fundamentals are little changed, lower prices make stocks more attractive, not less attractive. Diversification Remains Key Proper asset allocation is the one free lunch in the investment world. The magical effects of diversification – which help smooth returns over time – persist. During a massive selloff, stocks, bonds, commodities, real estate and other asset classes may all exhibit weakness, but this is a short-term phenomenon. Once we move beyond the urge to excessively sell in a panic, the benefits of diversification again become obvious. Avoid Emotional Reactions Your core portfolio needs to be sufficiently diversified (multiple assets classes with lower correlations) to give you the highest probability of achieving your goals for the reasons important to you. Stick to your core portfolio and look to rebalance so you remain on track long after you forget the scary headlines. Peter Lynch, one of the most successful investors of all time said, “The key to making money in stocks is not to get scared out of them.” -Paul R. Rossi, CFA  Risk is everywhere. Most of the time we don’t realize it. But it’s there. It’s always present and it’s everywhere. Let’s think about just a few things that seemly come out of nowhere, but probabilistically we should expect several "unexpected" life events to happen to us and the people we love. Here’s a short list of just some of the “risks” we might experience:

But most of us don’t think about all the things we will very likely experience in our lifetime. Some more serious than others, and depending on the nature of the circumstance, it can change our immediate plans or impact our life indefinitely. With the COVID-19 pandemic, people the world over received an awful reminder of how risky life really is. Most of us were affected all at once, the risk of our health, our freedom of movement, our incomes, and in a period of just 4 weeks, the stock market wiped out the previous 4 years of returns. The precipitous drop provided a hard reminder of the nature of risk and uncertainty. During the good times, it’s easy to forget that. What’s the best way to predict the future? The best way to predict the future, is to plan for it. How do we do that? Take a step wise approach to planning. Example: What are the various health issues that you or a family member might experience? What would you do in each case? Who would do what? How would it be paid for? etc. What are the various contingencies if you lose your job? How do you plan for this? What needs to be done today and in the near term to ensure that you can withstand this possibility? Never forget the future is always unknowable. But with some thoughtful planning, you can dramatically reduce the impact of these various risks. You can also reduce your anxiety by having a well-designed process for dealing with these life events. Part of reducing the stress that some of these risks can bring, is understanding that it’s part of living and even with proper planning, somethings are just out of our control. -Paul R. Rossi, CFA  You hear it all the time: You should make sure your retirement savings at least keep pace with inflation. But what is inflation and how does it really affect your retirement savings? Let's explore. In simple terms, inflation is defined as an increase in the general level of prices for goods and services. If inflation is relatively high, say 10%, as it was in the late 1970's and early 1980's, then a loaf of bread that costs $3.00 this year will cost $3.30 the next year, $3.63 in two years, and $4.00 in three years. Historically, inflation in the United States has averaged 3.24% from 1914 through 2021. However, over this more than 100-year period, it has varied quite a bit, it reached an all–time high of 23.70% in June 1920 and a record low of -15.80% in June 1921. In 2021, inflation went up every single month, which you no doubt already know. While moderately high inflation never is enjoyable, it’s still nowhere near what some other countries have experienced. Venezuela averaged 32.47% from 1973 until 2017, reaching an all–time high of 800% in December of 2016. Hyper-Inflation what Venezuela experienced is absolutely crippling.  So how does inflation affect your retirement savings? The answer is simple: Inflation decreases the purchasing power of your money in the future, lowering your standard of living. Consider this: at 3% inflation, $100 today will be worth $67.30 in 20 years, a loss of 1/3 its value. Said another way, that same $100 will only buy you $67.30 worth of goods and services in 20 years. And in 35 years? Your $100 will be reduced to just $34.44, which means you are losing almost 2/3 of your purchasing power. How is inflation calculated? Every month, the Bureau of Labor Statistics (BLS) calculates indexes that measure inflation: Consumer Price Index (CPI), a measure of price changes in consumer goods and services such as gasoline, food, clothing and automobiles. The CPI measures price change from the perspective of the purchaser. Producer Price Indexes (PPI), a family of indexes that measure the average change over time in selling prices by domestic producers of goods and services. PPI's measure price change from the perspective of the seller. How the Federal Reserve Attempts to Control Inflation Believe it or not, up until the early part of the 20th century, there was no central control or coordination of banking activity in the United States. In fact, the US was the only major industrial nation without a central bank until Congress established the Federal Reserve System in 1913 with the enactment of the Federal Reserve Act. With the Federal Reserve Act, Congress set three very specific goals for the Fed:

In order to help the Federal Reserve stabilize prices, Congress gave the Fed a very powerful tool: The ability to set monetary policy. And one way the Fed sets monetary policy is by manipulating short–term interest rates in an effort to control inflation. If the Fed believes that prevailing market conditions will increase inflation, it will attempt to slow the economy by raising short–term interest rates, reasoning that increases in the cost of borrowing money are likely to slow down both personal and business spending and therefore bring demand down which eases inflation. On the flip side: If the Fed believes that the economy has slowed too much, it can lower short–term interest rates in an effort to lower the cost of borrowing and stimulate personal and business spending. The most recent example being the pandemic, the Fed stimulated the economy by lower rates to help stave off a major recession. As you might imagine, the Fed walks a very fine line. If it does not slow the economy soon enough by raising rates, it runs the risk of inflation getting out of control. And if the Fed does not help the economy soon enough by lowering rates, it runs the risk of the economy going into recession. More recently the Fed has been targeting an "inflation at the rate of 2 percent (as measured by the annual change in the price index for personal consumption expenditures, or PCE) is most consistent over the longer run with the Fed's mandate for price stability and maximum employment." What Investors Need to Remember Understanding the powerful affect that inflation can have on your retirement nest egg, it is imperative that your long-term retirement strategies account for inflation. You should prepare for a decrease in the purchasing power of your dollar over time and should strongly consider assuming that inflation will be at least 3.24%. If you're wrong and you find that the inflation rate for the next 10, 20, or 30 years turns out to be less than 3.24%, then you'll be in even better shape than you had planned. For some things in life, it pays to be conservative. -Paul R. Rossi, CFA

Your portfolio may be designed to give you the best chance of achieving your financial goals but... Unfortunately, the market doesn’t care about your goals and your risk tolerance. Why? Because the Market Has a Mind of Its Own And a lot of the time, it can feel like the market is out to get you personally. Of course it's not, but it sure can feel that way. A key characteristic of a well-designed financial plan is the consideration of market volatility— and for good reason. It can shake even the most unflappable people. Building wealth over time may seem like a futile effort, but a well-designed financial plan can help you brave the ever-changing ebbs and flows of the markets. A Living, Breathing Plan A financial plan can give you a better idea of how to meet your goals. Any good financial plan is dynamic. People often see their financial plans as fixed in stone. You don’t want to wander too far away from your goals—but goals change. As your goals evolve, your plan must change too. Life changes can affect your financial goals as much as market changes. You may get a new job, enter a new tax bracket, buy a home, inherent money, need to care for an aging family member, have a baby or get a divorce, among the countless other life changes. What you can do is build a plan that accounts for the different scenarios that life could throw at you. What Should You Do? Your best first defense is to be aware of current trends by using the resources you have around you. With a prudent financial plan and the right supporting resources, you decrease the risk of being blindsided by unexpected factors that could negatively impact your financial situation. Focus on what you want to do with your money—not the trends and noise that could pull you off track. Having a clear vision of how you intend to invest and why. This is essential for making decisions that serve your larger financial goals. Knowing your investment philosophy will keep your eye on the big picture instead of market highs and lows. Another thing that can derail your best-laid plans: Y O U R E M O T I O N S Emotions can distract from goals by driving you to deviate from your plan. Instead of letting market gyrations dictate your actions, always look to your plan for guidance. A good plan that’s carefully laid out in partnership with a good financial professional should walk you through various simulations, so you make rational decisions well before emergencies arise. Sleep Better by Having a Financial Plan There’s no way to see into the future, but there’s one thing you can predict: Markets will always be unpredictable. It’s a financial advisor's job to collaborate with you on a thoughtfully designed plan that accounts for any issues that could derail your plan. This allows you to endure the inevitable bad times with confidence. So, if you have a plan, stick with it, and make sure it’s updated as your goals shift. If you don’t have a plan yet and are just focusing on investing advice, you’re missing out on the sense of security that a quality financial plan can provide. The best way to predict the future, is to prepare for it. -Paul R. Rossi  ,

Planning Ahead Can Help You Live Your Life on Purpose. The day before the AFC and NFC Championships were played on Sunday, ESPN broke the news that Tom Brady was retiring from football. Although, by the time Sunday night ended and football fans knew that the Los Angeles Rams and Cincinnati Bengals would play each other in Super Bowl LVI it was reported that Brady told the Tampa Bay Bucs he’s still not sure what he will do next year. He subsequently has confirmed that he is retiring, and many would argue at the top of his game. In his last year playing, he led the league in passing yards, passing touchdowns, and completions. He's won 7 Super Bowl Championships and is considered by many to be the best quarterback of all time. Impressive, and especially impressive for an athlete now in his 40's. When planning for retirement, whether you’re a decorated NFL quarterback or not, believe it or not, similar concerns can arise. Planning ahead can spell the difference between a successful retirement with enough money and being in a healthy mental state, or a stressful retirement with difficult decisions and limited options. As such, in a nod to Tom Brady’s seven Super Bowl rings, here are seven suggestions that anyone contemplating retirement should think about.

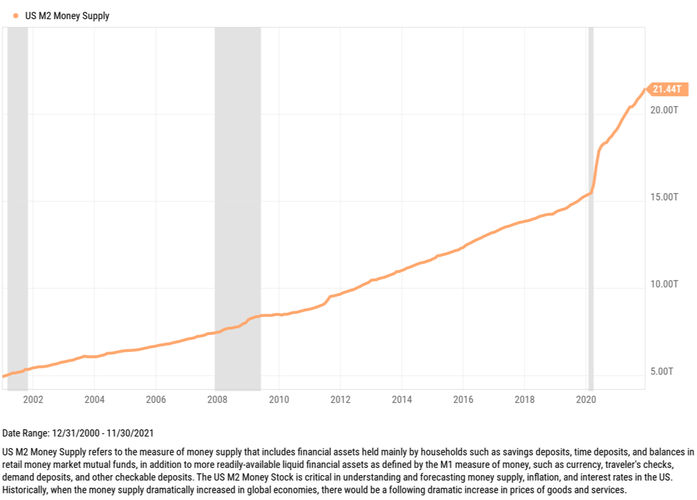

You may be close to retiring, but it doesn't mean that your planning stops, in fact it can become more important than ever. Talk to your financial advisor to make sure you are accurately planning for retirement, whatever that looks like for you, so you can sleep better at night. Especially on Sunday nights if there is no football for you. -Paul R. Rossi, CFA We live in tumultuous times—memories of an extraordinary financial crisis are still with us while we experience a once-in-a-century pandemic. Governments around the world are printing money at fabulous rates, including the United States. These circumstances cause us to ask, what causes inflation? In the simplest terms: Inflation is caused when too few goods are being chased by too much money. Understanding this, the chart below clearly shows why we are experiencing higher inflation than we have in decades, it depicts the Money Supply in the United States over the last 20 years. Do you notice anything about the money supply recently?  We should be surprised if we didn't have inflation after seeing this chart and understanding what it means.

-Paul R. Rossi, CFA  Market corrections happen about once every 19 months – and we’re at 19. After the stock market’s fantastic growth in 2021, some believe a pullback (or even a correction) may actually be healthy for the markets. Such a pullback is not horribly painful, by historical standards, and smart investors can cushion such a fall. Why is a market pullback or correction beneficial? You can think of a mild pullback or correction as a type of blow-off value; it allows pressure to be released to help avoid a much larger breakdown, and it can help prevent a large bubble from forming. Bubbles occur when stock prices get clearly out of line with the earnings potential of the underlying companies. We saw the consequence of that in the awful Technology crash of 2000-02 and Financial Crisis of 2008-09, when the markets collapsed, and some people lost half their wealth or more. Many companies didn’t survive. Certainly, market corrections never feel healthy when they occur. People get fearful as the market declines, the media fan the flames by giving investors reason after reason to be afraid. It very well may be, but most modest pullbacks are not the beginning of the next crash. Since 1950, the S&P 500 has experienced an intra-year peak-to-trough pullback of 5% or more in 67 out of 70 years. So roughly 93% of the time, a 5% correction has taken place from 1950- 2021. This could be considered normal market activity. The good news is many investors admit that a 5% pullback is manageably unpleasant, concerns expand when the market decline hits 10% or more. When is the Next Correction Coming? Here is what investors need to remember: the S&P 500 has nearly doubled in value since the market turmoil in March 2020. What has not happened since that time, however, is a selloff of at least 10% - that’s the definition of a market correction. In 29 of the past 50 years or 58% of the time the S&P 500 has experienced a 10% correction. Again, being that this happens more than 50% of the time, so this too should be considered normal. Since 1928, market corrections happen about once every 19 months. How to Prepare for a Correction Are you thinking: “I don’t think I can stomach a loss of 10%? Then that’s where the wisdom of diversification becomes apparent. Remember that the data above represent the historical performance of the S&P 500. A well-designed financial plan and portfolio can help ensure you have the proper asset allocation: a proper mix of Stocks (Small, Medium, Large, International, etc.), Bonds (Gov, Corp, Preferred, etc.), possibly some alternative investments, and Cash. Your portfolio should be designed to represent your tolerance for risk. So having proper diversification can keep you in the “manageably unpleasant” range. If not, you may need to reevaluate your risk tolerance to ensure you are not exposing your nest egg to a larger loss than you can endure. Although the recent market pullback will produce lots of fear, we’ve been here before. If you know what you own and why, then you should rest easy. -Paul R. Rossi, CFA  The CFA Institute through its research foundation recently published a 130+ page brief with insights from 25 years of Vertin Award recipients. These luminaries in the investment field come from a range of backgrounds, from Nobel Prize winners, distinguished professors, billionaire hedge fund managers, editors of prestigious academic journals, and authors of some of the most popular investment books ever published. Although their backgrounds vary widely, they have one thing in common: they have all made significant lifetime contributions in the field of finance. What is the Vertin Award? "The Vertin Award is given to intellectual leaders in the investment industry whose ideas are not only compelling in theory but meaningful in practice. The award winners are indeed exemplars of the CFA Institute mission to set the highest standards of ethics, education, and professional excellence for the ultimate benefit of society. It is fitting that this award is named for Jim Vertin, a dedicated volunteer and professional who recognized the potential to create a multiplier effect on the industry by connecting researchers with practitioners." - CFA Institute "None of us is as smart as all of us,” read the anonymous quote on the wall of James Vertin’s office. With that quote in mind, we can learn a lot from the collective wisdom of these Vertin winners. Below are a few of the recipient's and their notable comments. William Sharpe Noble Prize winner Professor Emeritus Stanford University

Marty Leibowitz CIO, TIAA and author of several seminal books and articles.

Andrew W. Lo Professor MIT

Clifford S. Asness President, AQR Management

Campbell R. Harvey Professor Duke University

Roger Clark President, Ensign Peak Advisors

Elroy Dimson Professor Cambridge & London Business School

Kenneth R. French Professor Dartmouth College

William Berstein Cofounder Efficient Frontier Advisors

William N. Goetzmann Professor Yale School of Management

Aswath Damodaran Professor NYU

In reading the insights from all 25 luminaries, several commonalities are found among them:

-Paul R. Rossi, CFA Download the entire Investment Luminaries and Their Insights below.

Following a budget is essential to financial health, but it can challenging for many people to create one and stick to it. Learn how to prioritize your spending when creating a budget and how to adapt expert advice to your financial goals. WHY BUDGET? Whether you’re working towards business, fitness, or financial goals, what matters most is creating a well-designed plan to get you from where you are today to where you want to be in the future. When it comes to meeting financial goals, a budget is one of the first building blocks of a sound financial plan. A budget shows how much income you’re bringing in and how much you plan to spend on different expenses. While you might not have much control over the inflow—household income—you can control the cash flowing out. Create a budget by:

Action step: Make adjustments to spending based upon on the 3 steps above. Ultimately, this will help you make financial decisions today that will help you meet tomorrow’s financial goals. WHAT MATTERS MOST When prioritizing spending goals, many families work towards building savings and investing while paying off debt.

A good financial advisor can help you to prioritize these goals based on your current financial situation, age, and other factors to help allocate the right amount to what's most important to you. Wondering where to find the money to build savings and pay off debt? Begin by tracking your spending. FOLLOW THE MONEY Once you are ready to create a budget, begin by determining how much after-tax money flows in and out of your household. This gives you an overview of how well you are meeting your fixed and variable expenses, and how much money you could earmark for your goals (above). While recording your after-tax income from earnings, investments, or other income is simple, recording your cash outflows is many times more complicated. You might have the best intentions to stick to a budget, but where does your money ACTUALLY go? For at least month week, track your spending using either a spending tracker app or old-fashioned paper and pencil. Identify the spending categories for every dollar flowing out of your accounts. This will show you when and where your spending occurs. Are there any surprises? Where could you cut back on expenses? Identify areas where you overspent, as well as opportunities to cut costs. WHAT A WELL-DESIGNED PLAN CAN PROVIDE Building a personalized household budget, prioritizing your spending categories, and crafting an actionable financial plan to help you meet your goals can:

Here's to getting ready for the New Year and a new way of thinking about your budget. It's much more than just numbers. -Paul R. Rossi, CFA  Sometimes I feel the fear of uncertainty stinging clear And I, I can't help but ask myself How much I let the fear take the wheel and steer It's driven me before And it seems to have a vague, haunting mass appeal But lately I'm Beginning to find that I should be the one behind the wheel Whatever tomorrow brings I'll be there With open arms and open eyes, yeah Whatever tomorrow brings I'll be there I'll be there So if I decide to waiver my chance To be one of the hive Will I choose water over wine And hold my own and drive? Oh It's driven me before And it seems to be the way, that everyone else gets around But lately I'm Beginning to find that when I drive myself, my light is found Whatever tomorrow brings I'll be there With open arms and open eyes, yeah Whatever tomorrow brings I'll be there I'll be there Would you choose water over wine? Hold the wheel and drive Whatever tomorrow brings I'll be there With open arms and open eyes, yeah Whatever tomorrow brings I'll be there I'll be there Lyrics and song by: Incubus Lead singer: Brandon Boyd explains, “The lyric is basically about FEAR, about being driven all your life by it and making decisions from fear. It’s about imagining what life would be like if you didn’t live it that way.” Not being ruled by Fear. I get it. It can be easier said than done. Because we are constantly being bombarded.  Market up 68% and GDP up over 3 trillion from when this magazine was issued in 2018  Market up over 265%, GDP up over 8 trillion from 2011.  The fear mongering isn't isolated to just the U.S.   Just to make sure they don't miss any region or country; they'll just name the whole world. We should all be living in a state of constant fear. Brandon Boyd of the band Incubus incapsulated it so well when he said, "It’s about imagining what life would be like if you didn’t live it that way.” Let's not only imagine it, let's live it. -Paul R. Rossi, CFA Click below to listen to the song bit.ly/IncubusDrive |

||||||||||