|

Do nothing. Huh? I repeat. Do nothing. What? Our whole lives we have been told and our own experience shows us by working hard, getting good grades, keeping busy, and pushing forward is almost a sure bet to getting ahead and grabbing the brass ring. In investing, the opposite is true. Which is why it makes it so hard to do. Doing nothing is almost always the surest way to success. As Warren Buffett says, "The Stock Market is designed to transfer money from the active to the patient." The best-performing mutual fund in the first decade of the 21st century was the CGM Focus Fund. During the ten years covering two recessions, the fund managed to generate an impressive 18% annualized return. What's even more amazing than this impressive return is that the typical investor in the fund actually lost almost -11% annually. You read that right, an 18% gain for the fund and an -11% loss to the investor. Huh? How is this even possible? Investors were doing exactly the opposite of what they should have been doing; they were buying high and selling low. Investors plowed into the fund when it was high, and when the fund waned a bit, they sold. This is one of the surest ways to go broke. And the CGM Focus Fund’s shareholders are not alone. Several other studies indicate that equity fund investors underperform across the board, on average, by over 6% per year between 1991 and 2010, according to Davis Advisors. Why does this happen? You can blame biology, we are preprogramed to want to "do something" when we are scared. And it made sense tens of thousands of years ago when we had to decide if a large animal might attack us. Quick action made sense, run now and live to hunt another day. This evolutionary response was critical to our survival as a species for thousands of years, unfortunately, our biology hasn't kept up with our current 'survival' needs. So where does this fear come from today? It comes from the media, so-called 'advisors', friends, family, co-workers, and neighbors. Most unsuccessful investors chase performance, engage in panic selling, and adopt myopic thinking encouraged by watching daily prices. Successful investors realize that no one can time the market consistently and therefore they ignore all the fear around them. They know the most important thing, is to have a plan, stick to their plan, and when others are selling, they do nothing. Warren Buffett said it best, "Investing is simple, but not easy." - Paul Rossi

0 Comments

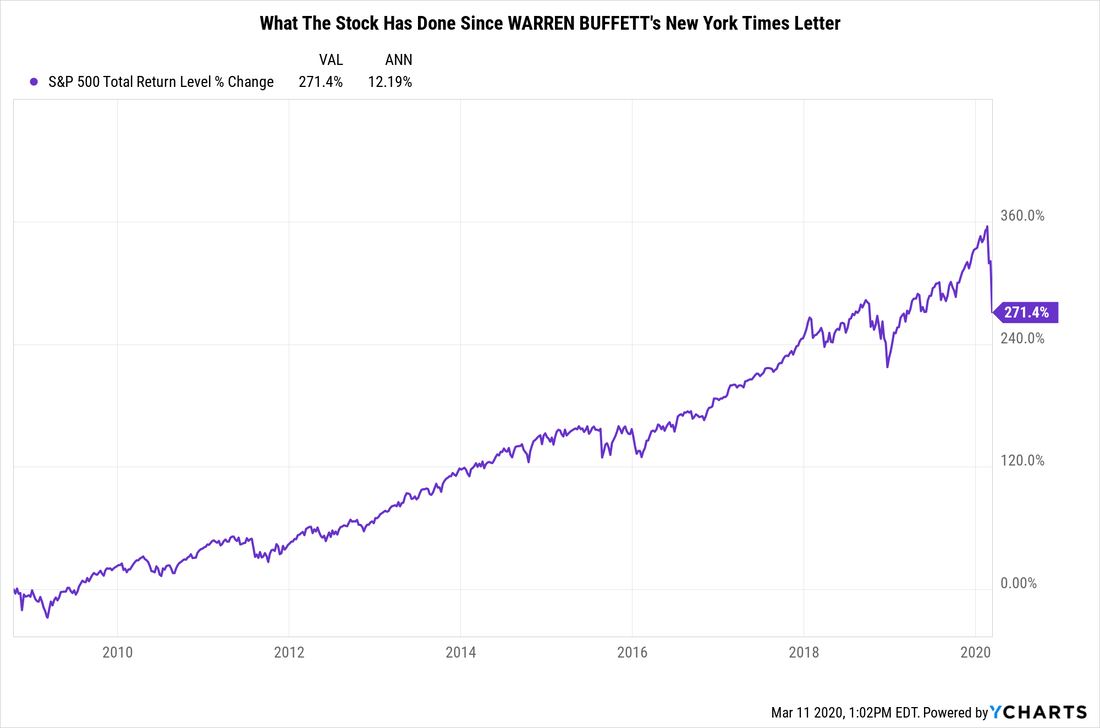

Below is a letter that Warren Buffett penned in THE NEW YORK TIMES during what would become known as the Global Financial Crisis. During these turbulent times, I think it's important to re-read what he wrote, it's sage advice for investors. By WARREN E. BUFFETT OCT. 16, 2008 THE financial world is a mess, both in the United States and abroad. Its problems, moreover, have been leaking into the general economy, and the leaks are now turning into a gusher. In the near term, unemployment will rise, business activity will falter and headlines will continue to be scary. So…I’ve been buying American stocks. This is my personal account I’m talking about, in which I previously owned nothing but United States government bonds. (This description leaves aside my Berkshire Hathaway holdings, which are all committed to philanthropy.) If prices keep looking attractive, my non-Berkshire net worth will soon be 100 percent in United States equities. Why? A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful. And most certainly, fear is now widespread, gripping even seasoned investors. To be sure, investors are right to be wary of highly leveraged entities or businesses in weak competitive positions. But fears regarding the long-term prosperity of the nation’s many sound companies make no sense. These businesses will indeed suffer earnings hiccups, as they always have. But most major companies will be setting new profit records 5, 10 and 20 years from now. Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month — or a year — from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So if you wait for the robins, spring will be over. A little history here: During the Depression, the Dow hit its low, 41, on July 8, 1932. Economic conditions, though, kept deteriorating until Franklin D. Roosevelt took office in March 1933. By that time, the market had already advanced 30 percent. Or think back to the early days of World War II, when things were going badly for the United States in Europe and the Pacific. The market hit bottom in April 1942, well before Allied fortunes turned. Again, in the early 1980s, the time to buy stocks was when inflation raged and the economy was in the tank. In short, bad news is an investor’s best friend. It lets you buy a slice of America’s future at a marked-down price. Over the long term, the stock market news will be good. In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497. You might think it would have been impossible for an investor to lose money during a century marked by such an extraordinary gain. But some investors did. The hapless ones bought stocks only when they felt comfort in doing so and then proceeded to sell when the headlines made them queasy. Today people who hold cash equivalents feel comfortable. They shouldn’t. They have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value. Indeed, the policies that government will follow in its efforts to alleviate the current crisis will probably prove inflationary and therefore accelerate declines in the real value of cash accounts. Equities will almost certainly outperform cash over the next decade, probably by a substantial degree. Those investors who cling now to cash are betting they can efficiently time their move away from it later. In waiting for the comfort of good news, they are ignoring Wayne Gretzky’s advice: “I skate to where the puck is going to be, not to where it has been.” I don’t like to opine on the stock market, and again I emphasize that I have no idea what the market will do in the short term. Nevertheless, I’ll follow the lead of a restaurant that opened in an empty bank building and then advertised: “Put your mouth where your money was.” Today my money and my mouth both say equities. Warren E. Buffett is the chief executive of Berkshire Hathaway, a diversified holding company.

|

||