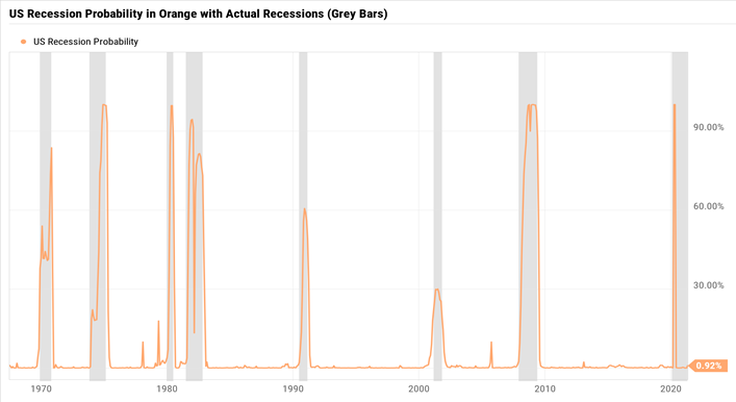

I'm not sure anyone can accurately predict recessions, the stock market, or anything else with 100% certainty...especially when it involves human interaction, but looking at key economic data might be able to provide some measured insight as to what the future may hold. Professor Jeremy Piger of the University of Oregon maintains a recession model that might just be able to do just that...provide some probabilistic numbers to what the economy might experience in the near-term. The chart below shows the last 50+ years of U.S. recessions (grey bars). In addition to the grey bars, the orange line is what the professor has produced, called the, "U.S. Recession Probabilities" (Chauvet and Piger) which uses smoothed probabilities of a recession in the U.S. It is calculated from a dynamic factor Markov-switching model using four economic inputs:

Over the last 50 years, the U.S. has experienced 8 recessions, including our most recent 2020 Covid recession. My personal prediction is that we will continue to experience recessions going forward...so if nothing else, get used to hearing that another recession is just around the corner, because it probably is. And if the last 50 years is any guide, we can expect a recession about every 6 to 7 years. While I don't advocate jumping in and out of the market based upon recent headline news, I do believe understanding where we are in the economic cycle can be valuable for a number of reasons. Here are just a few:

While there is no absolute silver bullet to forecasting certainty, the "U.S. Recession Probability" model is a bullet none-the-less, and it never hurts to have another tool in the tool belt. -Paul R. Rossi, CFA Click here to go to Dr. Piger's website and the Recession Probabilities Model.

0 Comments

Many people tend to think of the 529 Education Savings Plan as a good way to save for their children's or grandchildren's education. And they'd be right. But that's where it ends for most people...and this is a potentially costly oversight. It can be much more powerful than that. So what is the 529 and how does it work? A 529 is a tax-advantaged savings plan designed to help pay for education. How does it work? The plans are funded with after-tax dollars, but all money taken out, which includes all the investment gains, are tax-free as long it is spent on qualified education expenses, expenses like: tuition, administration fees, books, room and board, computer, internet access, lab fees, etc., the list is quite extensive. Even for modest savers, the growth in a 529 account which grow tax free can easily equate to tens of thousands of dollars or more of additional money if set up and used properly. How much can you contribute? You can contribute up to $15,000 (the annual gift tax limit) per beneficiary per year. So for a couple, that would be up to $30,000 per year. However, the law permits each account owner to pay up to five years’ contribution upfront without triggering gift taxes, which means a couple can contribute up to $150,000 per beneficiary in one fell swoop. Wow. This $150,000 can then grow tax free every year. In addition to this, there is no limit to the number of 529's a person or couple can set up. A couple with a large family, say with 10 grandchildren could set aside $1.5 million (10 accounts x 150,000 max contribution). This $1.5 million is then excluded from their estate for taxes purposes - which can have a dramatic impact. What happens if money is taken out for non-qualified expense or the original beneficiary (child/grandchild) doesn't go to college? The law permits the account holder to change beneficiaries as desired without penalty. This can be used should the original beneficiary not use the money. As an example, the beneficiary account could be transferred from child #1, to child #2, to grandchild #1, etc. So in essence, you can move money across generations without taxes as long as you don't hit gift tax exclusions. That's a potentially powerful estate planning tool. However, the power of the 529 account can still be very useful if the beneficiary doesn't use the money for educational purposes. While there is a 10% penalty and taxes are due for amounts taken out for non-educational purposes, even factoring this in, the math shows the 529 account balances can be worth tens of thousands or more than simply putting the money into a regular brokerage account. Some other notable highlights:

Although 529 plans have been around for years, many people do not appreciate the flexibility they offer. While it's a great savings tool for educational purposes, the accounts can be much more than that...it can be a part of a well thought out estate plan. - Paul R. Rossi, CFA  A well known valuation metric is the PE Ratio (Price / Earnings ratio). This is a measure of a company's share price (P) relative to the annual net income (E). The PE ratio shows current investor demand for a company share. A high PE ratio generally indicates increased demand because investors anticipate earnings growth in the future. The PE ratio has units of years, which can be thought of as the number of years of earnings required to pay back the purchase price. The PE ratio is often referred to as the "multiple" because it demonstrates how much an investor is willing to pay for one dollar of earnings. While the PE ratio is widely used, it is a bit of blunt instrument in terms of valuing a company. One of the biggest challenges of using the PE ratio is that it doesn't consider the growth in earnings of the company. If a company's earnings are rapidly growing, then its conceivable that it should trade at a higher PE ratio. So then the question becomes, what PE ratio is appropriate based upon the earnings and growth rate of the company? One solution to this problem is to look at the company's PEG ratio. The PEG Ratio (Price/Earnings to Growth ratio) illustrates the relationship between a company’s stock price, its earning per share, AND the company's growth rate. The PEG ratio consists of the PE ratio divided by the company's earnings growth rate. Using just the PE ratio makes high-growth companies look overvalued relative to others. By dividing the PE ratio by the earnings growth rate, the PEG ratio allows investors to compare companies in wildly different markets by factoring how growth rates affect valuations. By using the earnings growth in the denominator, it helps support the idea that growth is an important aspect to valuing a company. While not being set in stone, a company with a PEG ratio <1 can be considered undervalued. A company with a PEG ratio around 1 is considered fairly valued, and a company with a PEG ratio much >1 might be considered overvalued, all else being equal. Formula: PEG Ratio = PE Ratio / TTM (Trailing Twelve Months) Earnings Growth Rate* * Some analysts use a forward PE Ratio and use forecasted earnings growth, rather than trailing PE and historical earnings growth. Using historical numbers rather than forecasted numbers is typically more conservative if growth rates are increasing. Example: To illustrate a company's PEG Ratio, let's describe a hypothetical company called Blue Star trading at $167.42 per share. Blue Star EPS (Earnings Per Share) TTM for the following quarters were: 03/31/2020 - 5.12 06/30/2020 - 6.79 09/30/2020 - 7.53 12/31/2020 - 8.16 03/30/2021 - 8.98 Calculation:

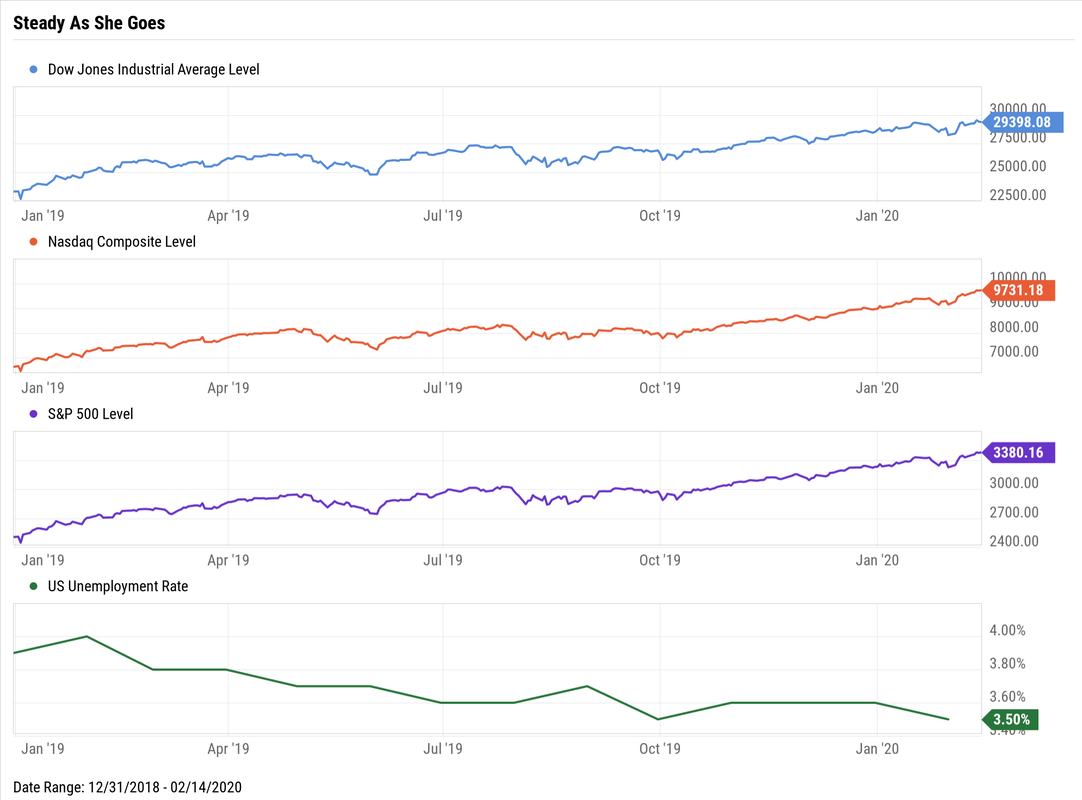

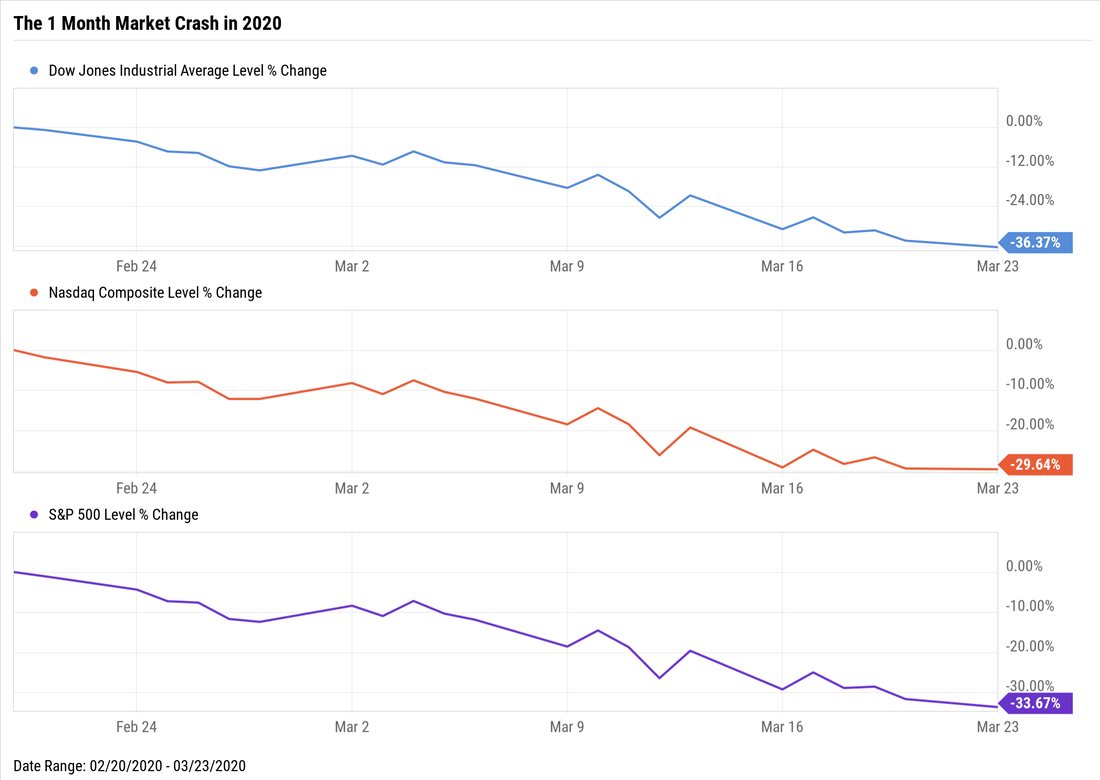

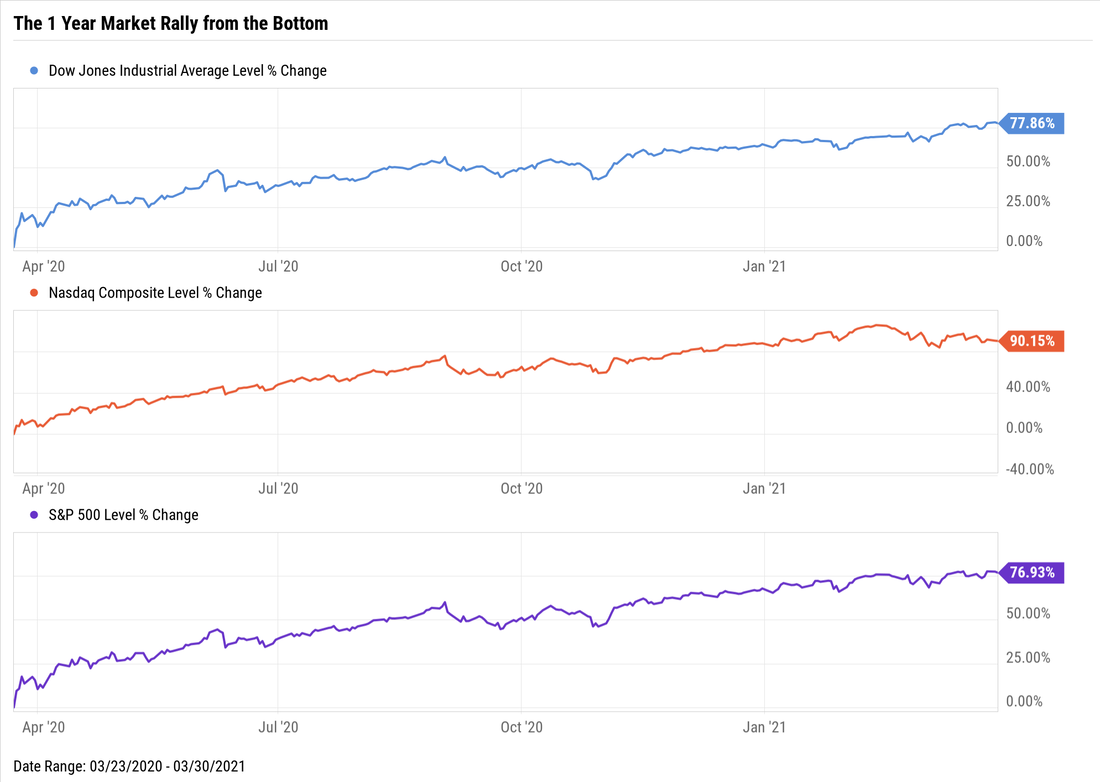

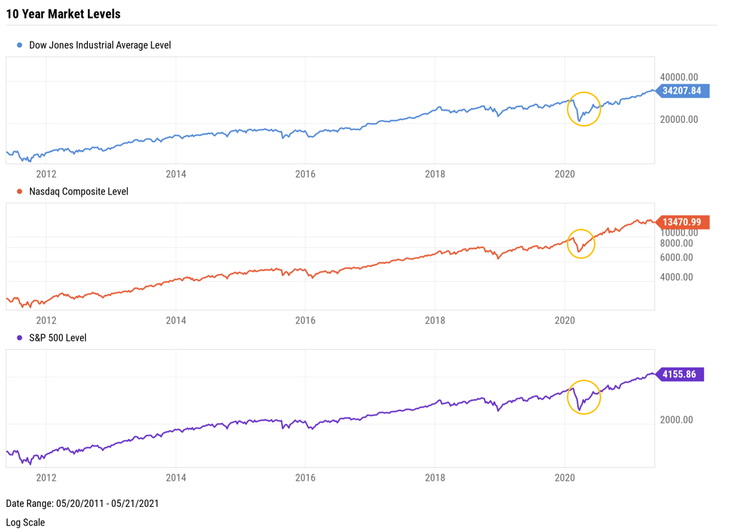

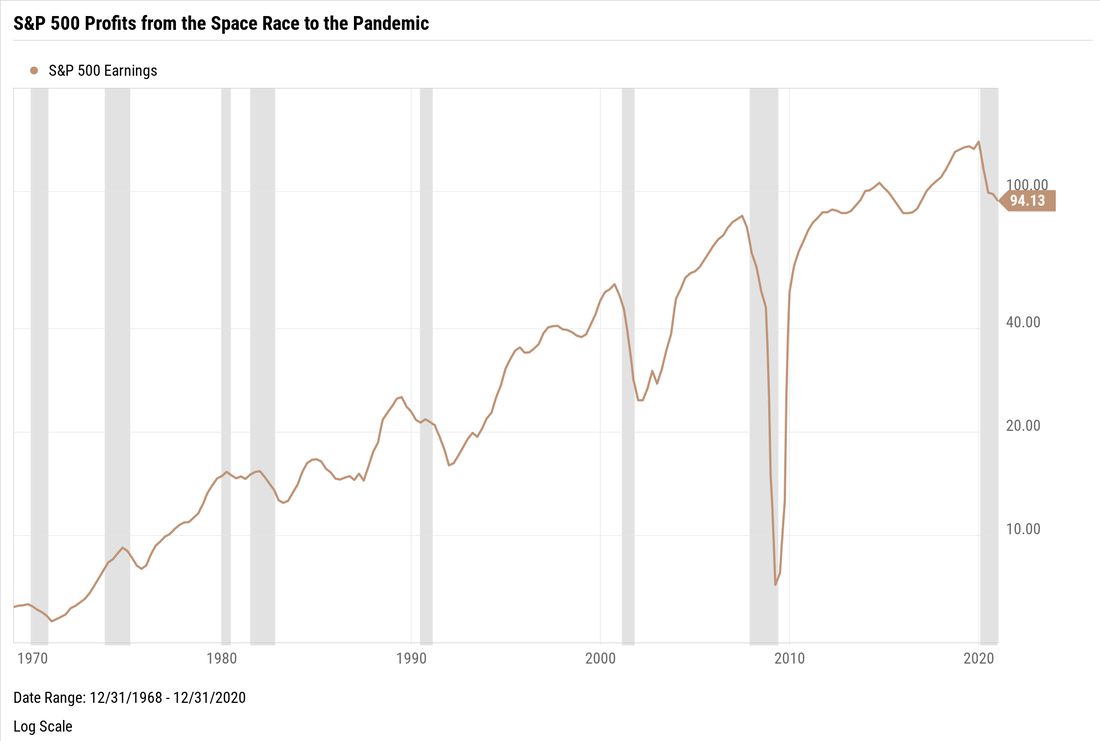

So in this case Blue Star could be considered significantly undervalued as the PEG ratio is .247, well below 1. Both the PE Ratio and the PEG Ratio are great tools that can be used to help value companies and/or compare companies in different industries, as the formulas are straight forward and the information needed is rather easy to ascertain. However keep in mind, calculating these ratios is more than likely just the beginning of the valuation process rather than the end. -Paul R. Rossi, CFA  Now that we have had some time to reflect back over the last year or so, I think it's important to keep things in proper perspective. Leading up to the Global Pandemic the markets had been performing quite well (see below).  Once it became clear that the world was facing a global pandemic, the United States and most of the rest of the world essentially shut down a large portion of their economies to stem the spread of the virus. And the markets reacted with veracity. Here's the 1 month market crash (Feb-March 2020) that will go down in history, for the dramatic speed in which the markets tanked.  However, the rally from the bottom (see below) will also surely go down in the history books as well. The markets are forward looking and determined that the economy would come back. They rallied well ahead of any vaccines being developed, let alone any being approved, and well before Covid rates began to come down.  When looking back over the past 10 years (see below), we can see that the market volatility in 2020 isn't too much out of the ordinary. The markets don't move in straight lines. Understanding this and not being rattled could be considered a modern day super power.  How about we go back and look at the profits of some of the largest U.S. companies from the time of the space race to the global pandemic (a little over 50 years). The gray bars show economic recessions. This chart is very telling...company profits are volatile, recessions are quite common, and most importantly companies continue to find ways to grow their earnings over time.  So what can we learn from all of this?

-Paul R. Rossi, CFA  As the economy expands and contracts, so do the financial performances of companies across the 11 stock sectors. The 11 sectors are listed below along with some of the industries within each individual sector.

When the outlook is positive, economically sensitive companies tend to perform better (at least historically), prompting investors to buy their shares. If the outlook turns bearish, investors might swap out of these types of companies and into companies that can better weather economic downturns. The practice of doing this is known as sector rotation. Cycles that can trigger sector rotations The economy goes through cycles, and sector rotations occur at each stage. The 3 most common cycles that investors follow are:

The Market Cycle (see below) typically moves ahead of the Economic Cycle, since investors make decisions in anticipation of the future. As such, the current market cycle stage can indicate which sectors will soon become market leaders: Market Cycle: Market Bottom What Happens: Systematic risk resulting from a poor economic backdrop brings the whole market lower. Investors prepare to rotate into more economically sensitive sectors. Best Performing Sectors Communication Services Consumer Staples Health Care Technology Utilities Market Cycle: Bull Market What Happens: The market bottom has passed, and the worst is over. As economic activity picks back up, so do share prices of cyclical stocks. Best Performing Sectors Consumer Discretionary Energy Industrials Materials Real Estate Technology Market Cycle: Market Top What Happens: Economic growth overheats, and interest rates rise. Investors prepare to rotate into more "defensive" sectors that are less economically sensitive. Best Performing Sectors Communication Services Financials Materials Market Cycle: Bear Market What Happens: Markets begin to drift from highs, and economic activity slows. As investors rotate out of cyclical sectors into defensive ones, selling activity accelerates the market decline. Best Performing Sectors Consumer Staples Health Care Utilities Market Cycles tend to lead Economic Cycles which is what happened both in the 2008 and 2020 recessions. In 2008, the S&P 500 peaked months ahead of US Monthly Real GDP's top. Stocks sold off in anticipation of a worsening economy. When COVID-19 became a pandemic in early 2020, the stock market was ahead of the 8-ball once again. Such is nature of both stock prices that discount future cash flows, and investors who want to be one step ahead. In both the Global Financial Crisis and the recent Covid-19 recession, the market rebounded well ahead of the fundamentals, which corresponds to the earlier statement, that Market Cycles lead Economic Cycles. Layered underneath the Market Cycle is the Economic Cycle. Because economic data is released less frequently, and investors price in their estimates beforehand, the Economic Cycle lags behind market movements. That said, it can provide solid confirmation of prevailing market trends. Sectors tend to perform differently based on the current Economic Cycle (see below) stage: Economic Cycle: Early Expansion What Happens: Rebounding GDP, Increased Production, Optimistic Consumer Sentiment, Reflationary environment, Low but Stable Interest Rates, Steepening Yield Curve Best Performing Sectors Communication Services Consumer Discretionary Industrials Materials Real Estate Technology Economic Cycle: Late Expansion What Happens: Tapering GDP, Tapering Production, Strong Consumer Sentiment, Growing Inflation, Spiking Interest Rates, Flattening Yield Curve Best Performing Sectors Consumer Discretionary Energy Financials Materials Economic Cycle: Early Recession What Happens: Declining GDP, Declining Production, Weakening Consumer Sentiment, High Inflation, Tapering Interest Rates, Flat or Inverted Yield Curve Best Performing Sectors Communication Services Consumer Staples Health Care Utilities Economic Cycle: Full Recession What Happens: Falling GDP, Falling Production, Pessimistic Consumer Sentiment, Deflationary environment, Falling Interest Rates, Normal Yield Curve Best Performing Sectors Consumer Staples Health Care Utilities Lastly, oversold and overbought indicators can be used to hone in on investment decisions with sometimes added precision. A very recent example: In late 2020, the Technology Sector triggered a commonly used overbought signal when its relative strength index (RSI) spiked. The sector immediately sold off by as much as 12.9% over the following months. Sector Rotation in Practice One argument for using a sector rotation strategy is that share prices of companies within each sector tend to move in the same direction. This is a natural effect of sector classification, companies with similar business models are grouped together as they can be economically affected by many of the same factors. At a minimum, investors can gain baseline exposure to a given sector’s sensitivities using individual stocks. Or, broader exposure can be secured using sector ETFs. An example is the relationship of crude oil prices with major airliners American Airlines, Delta Airlines, Southwest Airlines, and United Airlines, as well as United Parcel Service and FedEx. Despite operating in different industries, these industrial sector companies all benefit from lower oil prices, causing share prices to move higher when fuel costs decline. Investors can also use a top down approach and look to macroeconomic indicators to assess the current economic cycle stage. Once favorable sectors are identified, rotations are made out of unfavorable ones and into those that are poised to grow. Other Factors to Consider Some Important Warnings:

Finally, past performance isn’t always indicative of future results. -Paul R. Rossi, CFA  “Never confuse genius with luck and a bull market.” - John C Bogle “If you don’t recognize luck when it happens to you can fool yourself into thinking past performance was indicative of skill in a way that leads you to regrettable decisions.” - Morgan Housel “One lucky break, or one supremely shrewd decision—can we tell them apart?—may count for more than a lifetime of journeyman efforts.” -- Ben Graham "People often assume when a decision is followed by a good outcome, the decision was good, which isn't always true, and can be dangerous if it blinds us to flaws in our thinking." - Philip Tetlock “In a necessarily uncertain world, a good decision doesn’t necessarily lead to a good outcome, and a good outcome doesn’t necessarily imply a good decision or a capable decision maker.” - John Kay “The greatest trick the market plays on beginners is making you think luck is skill. It waits for you to double or triple down on your next bet and then it teaches you your first lesson.” - Ian Cassel "Making money through an early lucky trade is the worst way to win. The bad habits that it reinforces will lead to a lifetime of losses." - Naval Ravikant "During 'bull' markets, many investors tend to give themselves too much credit for favorable results and to give insufficient credit to the positive environment that played a large role in creating the results. This can lead to overconfidence on the part of the investor and resulting mis-assessment of risks." - Ed Wachenheim "Just because you made money doesn’t mean you were right, and just because you lost money doesn’t mean you were wrong. It is all a matter of probabilities. If you take a bet that has an 80% probability of winning and you lose, it doesn’t mean it was a wrong choice.” - Tom Claugus "Every once in a while, someone makes a risky bet on an improbable or uncertain outcome and ends up looking like a genius. But we should recognize that it happened because of luck and boldness, not skill." - Howard Marks “The absence of loss does not necessarily mean the portfolio was safely constructed. So, risk control can be present in good times, but it isn’t observable because it’s not tested. Ergo, there are no awards. Only a skilled and sophisticated observer can look at a portfolio in good times and divine whether it is a low-risk portfolio or a high-risk portfolio.” - Howard Marks “The correctness of a decision can’t be judged from the outcome. Nevertheless, that's how people assess it. A good decision is one that’s optimal at the time it’s made, when the future is by definition unknown. Thus, correct decisions are often unsuccessful, and vice versa.” - Howard Marks "It is all about believing in yourself and not confusing a bull market with brilliance and a bear market with stupidity.. markets are markets. You can't take it personally." - Mark Kingdon “Just because you did something that worked doesn’t mean that it wasn’t risky or wasn’t smart.” - David Abrams "Numbers can be very misleading because very smart people can struggle and very mediocre people can excel for periods of time." - Jim Chanos "The mere fact an aggressive strategy wins in a winning period doesn't prove it's the right strategy for all periods." - Howard Marks "Just because you buy a stock and it goes up does not mean you are right. Just because you buy a stock and it goes down does not mean you are wrong." - Peter Lynch “One thing about investing is, I think it’s good not to think that one is a genius, because the stock market will bury you.” - Jean Marie Eveillard “It’s dangerous to think you know too much and have your ego all involved in showing how smart you are and all that. It’s not an accident we use all of this self-deprecatory humor at Berkshire. It’s required for sanity. It really is.” - Charlie Munger "When you are having a good run of it, you are not as smart as you think you are, and when you are struggling with it, you are typically not as dumb as you look." - John Harris “Ego is the enemy of investing.” - Jake Rosser “Anytime that you think you’ve become a financial genius – when, in fact, you simply have had good luck to turn a profit – it is time to sit back and do nothing for a while. If you stumble upon success in a bull market and decide that you are gifted, stop right there. Investing at that point is dangerous, because you are starting to think like everybody else. Wait until the mob psychology that is influencing you subsides.” - Jim Rogers “I have seen a lot of people who confuse money with brains and more than a few traders who develop an unbounded view of their own infallibility … and usually such hubris precedes some sort of market retribution. I am sure that most of us in this room have seen that biblical injunction of pride coming before the fall strike someone near us in the trading world — if not hit us directly between the eyes.” - Bruce Kovner “Success tends to breed confidence and then, eventually, overconfidence — and why would one examine what he’s doing when it’s so successful, even if it’s silly!” - David Polen "Any investor can chalk up large returns when stocks soar....In a bull market, one must avoid the error of the preening duck that quacks boastfully after a torrential rainstorm thinking its paddling skills have caused it to rise in the world. A right-thinking duck would instead compare its position after the downpour to that of the other ducks on the pond." - Warren Buffett "Good decision-making can lead to bad outcomes and vice versa. If we believe that we predicted the past better than we did, we may also believe that we can predict the future better than we can." - Peter Bevelin "The riskiest thing is getting lucky - a false positive. You have a positive result, but your process was poor. That's the most dangerous because, after a few false positives, you typically go bigger, and that leads to the old saying of "succeed small, fail big.” So we think about this pretty carefully." - Ken Shubin Stein "We have talked about how a sound investment process likely leads to a good investment result. A good result, though, says nothing about whether the process involved was a good one, and, thus, whether or not the success might be replicable." - Seth Klarman "In a bad year, defensive investors lose less than aggressive investors. Did they add value? Not necessarily. In a good year, aggressive investors make more than defensive investors. Did they do a better job? Few people would say yes without further investigation. A single year says almost nothing about skill, especially when the results would be expected on the basis of the investor's style." - Howard Marks “Short-term performance is an imposter." - Howard Marks "One of the allures of this business is that sometimes the greatest ignoramus can do well. That is unfortunate because it creates the impression that you don't necessarily need any professionalism to do well, and that is a great trap." - Michael Steinhardt “Return alone—and especially return over short periods of time—says very little about the quality of investment decisions.” - Howard Marks “A year is far too short a period to form any kind of an opinion as to investment performance, and measurements based on six months become even more unreliable. One factor that has caused some reluctance on my part to write semi-annual letters is the fear that partners may begin to think in terms of short-term performance which can be most misleading. My own thinking is much more geared to five-year performance, preferably with tests of relative results in both strong and weak markets.” - Warren Buffett 1960 Partnership letter "Short-term performance measurements are meaningless, and it is impossible to forecast with any certainty what the relative performance of a manager will be in any given year. In fact, even a several-year span can be misleading, as a manager may be able to achieve above-average results by owning very high-risk stocks in a generally rising market (as we had in the 1960s) but be virtually wiped out in the same class of stocks in a bear market. The only true test of a money manager's ability is if he can obtain above-average results over a full cycle that includes both bull and bear markets. A great investment manager must be ‘a man for all seasons’." - Barton Biggs "It can take years to judge the quality of an investment decision. Those who believe that they are quite witty because of a few years of strong performance – for a stock or for the whole portfolio – should develop a strong auto-skepticism reflex." - Francois Rochon “If I had to choose a great single fallacy of investing, it’s that when a stock’s price goes up, you’ve made a good investment. People take comfort when their purchase at $5 goes to $6, as if that proves the wisdom of the purchase. Nothing could be further from the truth.” - Peter Lynch “One reason the financial industry mints so many extraordinary egos is because it’s easy to take personal credit for what works and claim to be a victim of what doesn’t. Industrial engineers can’t simply be in the right place at the right time, or blame their failures on the Federal Reserve. But investors can, and do. An iron rule of investing is that almost nothing is certain and the best we can do is put the odds of success in our favor. Since we’re working with odds – not certainties – it’s possible to make good decisions that don’t work, bad decisions that work beautifully, and random decisions that may go either way. Few industries are like that, so it’s easy to ignore. But it’s a central feature of markets. Unless you’ve enjoyed a period of success that you realize you had nothing to do with, or can admit that a long period of loss was due to your own mistake, you’ll have a hard time grasping reality in a way that lets you do at least the average thing when everyone else is losing their minds.” - Morgan Housel “The stock market provides an uneven feedback loop for investment decisions. This unusual economic microcosm may sometimes reward poor decisions and often penalizes good ones… When a blackjack player receives a 3 after he hits on 18, he may celebrate a victory, but clearly the decision to hit was incorrect, based on all available information at the time. Good portfolio managers have this concept ingrained in their thinking They realize positive outcomes are sometimes confirmation of a good decision, and sometimes they are not. What matters is process.” - Brian Bares -Paul R. Rossi, CFA  Over the weekend (Saturday May 1st), Warren Buffett and Charlie Munger held their annual shareholder meeting for Berkshire Hathaway, and as usual, it was a filled with timeless wisdom for investors and non-investors alike. I highly recommend you listen or watch the entire meeting, as both Warren and Charlie continue to dazzle us with their insightful thoughts and ideas. If you don't have 3+ hours to watch the meeting I would recommend you read the short conversation (see below) between author Robert Hagstrom and Lauren Foster of the CFA Institute. If you've ever Googled "Warren Buffett" and "books to read," you'll find Robert Hagstrom's first book on the list, "The Warren Buffett Way." The Warren Buffett Way spent five months on the New York Times bestseller list in 1994 and '95, and is routinely included in lists of the best books to read on the Oracle of Omaha. Robert is a CFA charter holder and a Senior Portfolio Manager at Equity Compass, where he launched the global leaders portfolio. He also serves as Chairman of the Investment Management Committee for Stifle Asset Management. A recent conversation between Robert and Lauren Foster of the CFA Institute is all about this concept of a money mind. What exactly is a money mind? What are the components? And importantly for investors, can they be learned? Below is a quick excerpt between Lauren Foster of the CFA Institute and Robert Hagstrom.

Click the PDF below to get the entire conversation and learn more about the Money Mind. -Paul R. Rossi

Understanding and successfully following the inherited IRA rules can be a bit confusing, but it doesn’t take away from the fact that it’s vitally important to get it right. As there is a 50% penalty of the amount you should have distributed if you don't take the proper RMD's (Required Minimum Distributions). Never forget: The IRS wants its money and the IRS gets paid when you distribute money from an IRA account. As a result of the SECURE Act that was passed in late 2019, there are now essentially two sets of rules (and some additional sub rules) for inherited IRAs. How do you determine which set of rules to follow depends on two things:

If the original IRA account holder passed away in 2020 or later If the IRA owner died in 2020 or later, we first must determine whether the beneficiary is an “eligible beneficiary” or not. Eligible beneficiaries include:

If the beneficiary is an “eligible beneficiary,” then the more favorable “old” rules apply – go to the section that begins with “Eligible beneficiaries and deaths that took place in 2019 or earlier” below. If the beneficiary isn’t considered an eligible beneficiary, then the “New” Inherited IRA Rule applies – see below. The “New” Inherited IRA Rule If the beneficiary is not an “eligible beneficiary” from above, the new rule applies. What’s the new rule say? It says that the account must be completely distributed within 10 years of the original owner’s death. The distributions do not, however, require that they be taken evenly over those 10 years. For example, if you wanted, you could take no distributions for the first 9 years, then distribute everything in year 10. However, the account must be fully distributed by 12/31 of the 10th anniversary year of the original owner’s death. Eligible beneficiaries and deaths that took place in 2019 or earlier The “old rules” discussed in the remainder of this article apply in situations in which either:

Under the “old rules,” there are still actually two sets of rules: one set of rules that applies if the deceased owner was your spouse, and another set for any other designated beneficiary. With this, the rules are different depending on the relationship to the original account holder:

1. Inherited IRA: Spouse Beneficiary As a spouse beneficiary, you have two primary options:

Note: There is no deadline on a spousal rollover. Should you want to, you can own the account as a spousal beneficiary for several years, then elect to do a spousal rollover. If you do a spousal rollover, from that point forward it’s just a normal IRA (i.e., it’s just like any other IRA that was yours to begin with), so all the normal IRA rules apply, whether Roth or traditional. If you continue to own the account as a spousal beneficiary, the rules will be similar to normal IRA rules, but with a few important exceptions. No 10% Penalty First, you can take distributions from the account without being subject to the 10% penalty, regardless of your age. So if you expect to need the money prior to age 59.5, this is a good reason not to go the spousal rollover route — at least not yet. (As mentioned above, there’s no deadline on a spousal rollover.) Withdrawals from Inherited Roth IRA Second, if the inherited account was a Roth IRA, any withdrawals of earnings taken prior to the point at which the original owner would have satisfied the '5-year rule' will be subject to income tax (though not the 10% penalty). Spouse Beneficiary RMDs Third, you’ll have to start taking required minimum distributions (RMDs) in the year in which the deceased account owner would have been required to take them. (If the original owner — your spouse — was required to take an RMD in the year in which he/she died, but he/she had not yet taken it, you’re required to take it for him/her, calculated in the same way it would be if he/she were still alive.) Your RMD from the account will be calculated each year based on your own remaining life expectancy from the 'Single Life' table in IRS Publication 590-B. 2. Inherited IRA: Non-Spouse Beneficiary When you inherit an IRA as a non-spouse beneficiary, the account works much like a typical IRA, with three important exceptions. No 10% Penalty Distributions from the account are not subject to the 10% penalty, regardless of your age. (This is the same as for a spouse beneficiary.) Withdrawals from Inherited Roth IRA If the inherited account was a Roth IRA, any withdrawals of earnings taken prior to the point at which the original owner would have satisfied the 5-year rule will be subject to income tax, though not the 10% penalty. (This is also the same as for a spouse beneficiary.) Non-Spouse Beneficiary RMDs Each year, beginning in the year after the death of the account owner, you’ll have to take a required minimum distribution from the account. (If the account owner was required to take an RMD in the year of his death but he had not yet taken one, you’ll be required to take his RMD for him, calculated in the same way it would be if he were still alive.) The rules for calculating your RMD are similar (but not quite identical) to the rules for a spousal beneficiary. Again, your first RMD from the account will be calculated based on your own remaining life expectancy. However, in following years, instead of looking up your remaining life expectancy again (as a spousal beneficiary would), you simply subtract 1 year from whatever your life expectancy was last year.** For example, imagine that your father passed away in 2018 at age 65, leaving you his entire IRA. For 2018 (the year of death), you have no RMD. On your birthday in 2019, you turn 30 years old. According to the Single Life table, your remaining life expectancy at age 30 is 53.3 years. As a result, your RMD for 2019 would have been equal to the account balance as of 12/31/2018, divided by 53.3. For 2020, if it weren’t for the CARES Act eliminating RMDs for 2020, your RMD would have been equal to the account balance at the end of 2019, divided by 52.3. (But because of the CARES Act, the RMD for 2020 would be zero.) In 2021, the RMD will be the 12/31/2020 balance, divided by 51.3. Important exception: if you want, you can elect to distribute the account over 5 years rather than over your remaining life expectancy. If you elect to do that, you can take the distributions however you’d like over those five years — for example, no distributions in years 1-3 and everything in year 4. Successor Beneficiary RMDs If a beneficiary dies before the account has been fully distributed, the new inheriting beneficiary is known as a successor beneficiary. If the original account owner died in 2020 or later and the original beneficiary (i.e., the first person to inherit the IRA) was a “non-eligible” beneficiary, then the successor beneficiary will have to keep using the same distribution schedule. That is, the successor beneficiary will have to distribute the account within 10 years of the original owner’s death. Conversely, if the original account owner died before 2019 and/or the original beneficiary was an “eligible” beneficiary, then the successor beneficiary will have to distribute the account over 10 years, but it’s a new 10-year period, beginning with the date of the original beneficiary’s death (rather than beginning with the date of the original owner’s death). Tips for Non-Spouse Beneficiaries

3. Inherited IRA: Multiple Beneficiaries If multiple beneficiaries inherit an IRA, they’re each treated as if they were non-spouse beneficiaries, and they each have to use the life expectancy of the oldest beneficiary when calculating RMDs. This is not a good thing, as it means less ability to “stretch” the IRA. However, if the beneficiaries split the IRA into separate inherited IRAs by the end of the year following the year of the original owner’s death, then each beneficiary gets to treat his own inherited portion as if he were the sole beneficiary of an IRA of that size. This is a good thing, because it means that:

To split an inherited IRA into separate inherited IRAs:

Some parting thoughts When you inherit an IRA, it is imperative that you take the time to learn the applicable rules before doing anything. Don’t move the money or make any changes until you understand all of the potential implications because simple administrative mistakes can be very costly. -Paul R. Rossi, CFA  Before we can answer that, lets first define what a “value stock” is and what is considered a “growth stock.” Keep in mind, the following definitions are not hard and fast rules, but rather broad ideas/principals, and investors will have slightly different definitions or thresholds as to which bucket a stock should be placed. Value Stock Some key characteristics of value stocks are-

Growth Stock The key characteristics of growth stocks are-

In addition to looking at and understanding the value vs. growth question, investors also need to consider whether to purchase individual stocks, mutual funds, or ETF’s to implement these strategies. Some general rules of thumb- Growth may be right for you if you’re comfortable with larger price movements and you aren’t in need of current income (by way of dividends). However, you might prefer value if you’re looking for more stable investments that regularly pay dividends. There’s also a case to be made for including both value and growth in your portfolio to smooth out times of volatility and capture the best of both worlds. Value vs Growth, which is better for you? Your preference for, or belief in, value vs. growth typically comes down to your investment objectives, risk tolerance, and time horizon. You may prefer to achieve exposure to growth or value, or some combination of both. Again, these are broad strokes, the devil is in the details, so doing a thorough analysis (as always) should be done prior to any investment decision. -Paul R. Rossi, CFA  Tokugawa Crest The United States civil war lasted 4 years (1861-1865) and caused more than 1 million casualties. The war accounted for more American deaths than in all other U.S. wars combined. Now imagine a civil war lasting well over a 100 years. The period in Japan known as the Sengoku period from 1467 – to roughly 1615 was just such a period. During this time, Japan was in near constant civil war, causing social upheaval, and never-ending political instability. Many regional daimyo (local lords) were continually fighting, vying for land, power, and control during this period, costing countless lives. In the late 1560’s Oda Nobunaga, a powerful daimyo began to consolidate and control a large portion of central Japan through a series of successful sieges and battles. And for the first time in over 100 years, he brought some stability to this part of Japan. While his ultimate goal was to unify all of Japan under his control, he succeeded in conquering a portion of Japan before his untimely death, but was unable to accomplish his ultimate goal. In 1582, taking over where Nobunaga left off, Toyotomi Hideyoshi a top general of Nobunaga, over the next decade continued the process of unifying of Japan, ultimately bringing relative stability to Japan. However, in 1598 Hideyoshi died without leaving an heir who could immediately take over, leaving a vacuum in power that many wanted to fill. Following Hideyoshi’s death, Tokugawa Ieyasu, a former vassel of Hideyoshi, masterfully positioned himself to seize power and eventually lead the way for him to become Shogun (supreme leader) of Japan, bringing peace to a country that had only known war. He was able to complete the unification of Japan and outlast all the other great leaders of the time by employing several qualities that enabled him to rise to power. He was both careful and bold—at the right times, and in the right places. He was also calculating and subtle; Ieyasu switched alliances when he thought he would benefit from the change. Serving along-side and under both Nobunaga and Hideyoshi, he understood the power of patience. He acted only when the odds were in his favor. Under his consolidation of power, he used his remaining years to create and solidify what became known as the Tokugawa shogunate which would rule Japan for the next 260 years. He is thought to have fought in 90 battles throughout his lifetime. Later in life he took to introspection and said, “The strong ones in life are those who understand the meaning of the word patience. Patience means restraining one's inclinations. There are seven emotions: joy, anger, anxiety, adoration, grief, fear, and hate, and if a man does not give way to these, he can be called patient. I am not as strong as I might be, but I have long known and practiced patience. And if my descendants wish to be as I am, they must study patience.” Some things just take time. Knowing when to act and when not to act is a powerful skill. Investing can be thought of similarly. Warren Buffett has said, “Time is the friend of a wonderful company, and the enemy of a mediocre one,’ and “You can’t produce a baby in one month by getting nine women pregnant.” Warren Buffett also understands the value of patience. Understanding and appreciating these two quotes by arguably the greatest investor of all time and employing the active patience Ieyasu was so masterfully able to do, will serve you well. -Paul R. Rossi, CFA  What is Bushidō? Bushidō can be translated to mean, "the way of the warrior." It is a Japanese moral code concerning Samurai behavior, attitudes, and lifestyle. Bushido can be thought of as an overarching term for all the codes, practices, philosophies, and principles of Samurai culture. Samurai were the warrior class in Japan that enjoyed high prestige, special privileges, and many military historians consider them to be some of the best swordsmen the world has ever seen. This “code of conduct” has a long history in Japan which began to take shape with the rise of the warrior caste to power over a thousand years ago during the Heian period (794 -1185) and it was more formally defined over subsequent dynasties and applied into law during the Edo period (1603 - 1867). So what is the Bushido code of moral conduct? Bushido formalized earlier Samurai moral values and ethical code, most commonly stressing a combination of these Eight Primary Principles

These principals were required to be observed in order to become a Samurai and were expected to be mastered. The Samurai ruled Japan for over a thousand years using these principals to live, how might you incorporate them in your life? Strive to live (and invest) the Bushidō way. -Paul R. Rossi, CFA  In the the spirt of celebrating St. Patrick's Day today, here are some tidbits to chew on in between your green beer and corn beef. While many times we think we know the truth, sometimes the truth is quite different from what we think it is. Who St. Patrick wasn't:

Here's who he was:

In fact, many times the truth is stranger than what you might think. Let me explain. The vast majority of the stock of individual companies since 1926 have returned less 1 month US-Treasury Bills. Read that last sentence again. How is this possible when the fact that stock markets provide long-term returns that exceed the returns of low risk investments, such as government obligations? This has been extensively documented for the US stock market as well as for many other countries around the world. We all have read that stock returns are greater than super safe US government bonds. That's why we invest in stock, to earn more than the low rates in savings accounts and short-term bonds. So prepare for your mind to be blown away. It gets even worse, the single most frequent outcome (when returns are rounded to the nearest 5%) observed for individual stock over their full lifetime is a loss of 100%. Read that last sentence again and let it sink in. A 100% loss is the most common outcome for individual stock. The median time that a stock is listed is seven-and-a-half years. What does this mean? Companies don't last long. The fact that the overall stock market generates long-term positive returns could be considered a puzzle. While the majority of individual stocks fail to even match Treasury bills, the positive returns can be attributed to how the distribution of individual stock returns. The returns are positively skewed. Simply put, large positive returns of a very few stocks offset the majority of the losers. The data shows that approximately 25,300 companies that issued stock appearing in the CRSP common stock database since 1926 are collectively responsible for lifetime shareholder wealth creation of nearly $35 trillion (as of December 2016). However and amazingly, just 5 firms (Exxon Mobile, Apple, Microsoft, General Electric, and IBM) account for 10% of this total wealth creation.

So when you are done drinking your green beer and start thinking about which companies to invest in, keep in mind that "picking winners" is extremely difficult, so you better hope you have some luck of the Irish on your side. - Paul R. Rossi, CFA Here is a link to the published paper by professor Dr. Hendrik Bessembinder that this article references.   I can't think of any other 97 year-old-person I'd rather listen to than Charlie Munger. Billionaire Charlie Munger is one of the most successful investors of all time and he also happens to be Warren Buffett's partner for over 50 years.

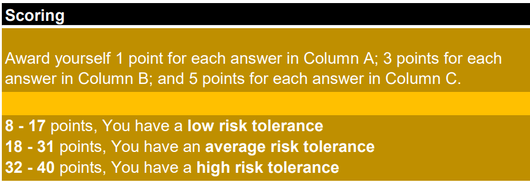

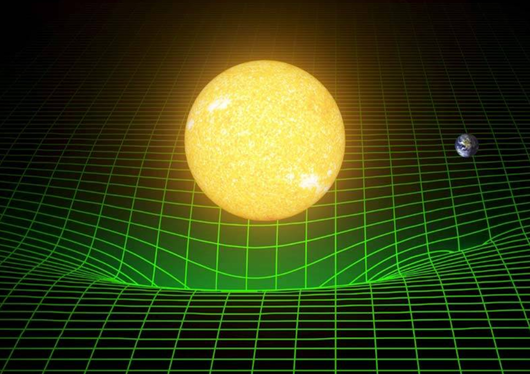

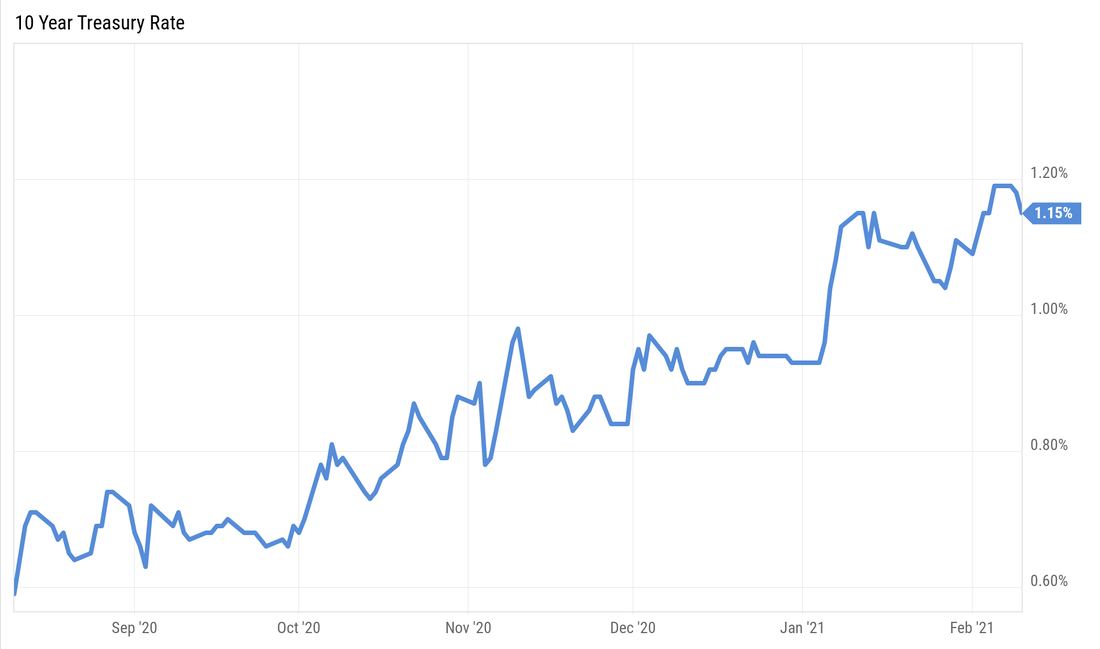

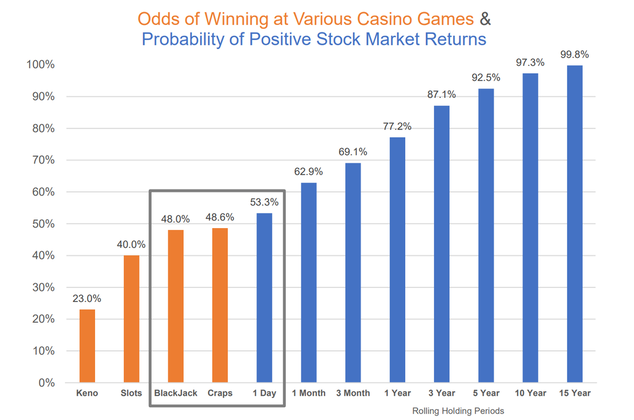

Charlie Munger is Vice-Chairman of Berkshire Hathaway, on the Board of Costco, and Chairman of the Board of the Daily Journal Corporation (a newspaper publisher and software developer). Of course Mr. Munger is well-known for his investing prowess, but he is equally respected for his thoughts outside of investing. Investors and just about everyone would be well advised to follow many of the principals and ideas Mr. Munger has shared over the years. This content comes from Theron Mohamed at Markets Insider. Below are lightly edited comments from yesterday's Daily Journal annual shareholder meeting covering his thoughts from Bitcoin to marriage, and many things in-between. Enjoy...and here's to soaking up some of Mr. Mungers worldly wisdom. Market Speculation "These things do happen in a market economy, you get crazy booms. I've been around for a long time and my policy's always been to just ride it out." "A lot of investors are buying stocks in a frenzy, frequently on credit, because they see them going up. That's a very dangerous way to invest." "Shareholders should be more sensible and not crowd into stocks and just buy them just because they're going up and they like to gamble." "I think it must end badly but I don't know when." GameStop "That's the kind of thing that can happen when you get a whole lot of people who are using liquid stock markets to gamble the way they would bet on racehorses." "The frenzy is fed by people who are getting commissions and other revenues out of this new bunch of gamblers. When things get extreme you have things like that short squeeze." "It's very dangerous and it's really stupid to have a culture which encourages as much gambling in stocks by people who have the mindset of racetrack bettors. Of course that is going to cause trouble, as it did." Robinhood and Trading Apps "If you're selling people gambling services where you make profits off the top like many of these new brokers who specialize in luring gamblers in, it's a dirty way to make money and I think we're crazy to allow it." "[Wretched excess in the financial system] is most egregious in the momentum trading by novice investors lured in by new types of brokerage operations like Robinhood. All of this activity is regrettable, civilization would do better without it." "Human greed and the aggression of the brokerage community creates these bubbles from time to time. Wise people just stay out of them." "When you pay for order flow, you're probably charging your customers more in pretending to be free. It's a very dishonorable, low-grade way to talk. Nobody should believe that Robinhood's trades are free." Stock Valuations When Interest Rates Are Low "Everybody is willing to hold stocks at higher price-earnings multiples when interest rates are as low as they are now. I don't think it's necessarily crazy that good companies sell at way higher multiples than they used to." "On the other hand, I didn't get rich by buying stocks at high price-earnings multiples in the midst of crazy, speculative booms, and I'm not going to change." SPACs "The world would be better off without them. This kind of crazy speculation, in enterprises not even found or picked out yet, is a sign of an irritating bubble. The investment-banking profession will sell shit as long as shit can be sold." Bitcoin "I don't think bitcoin is going to end up the medium of exchange for the world. It's too volatile to serve well as a medium of exchange." "It's really kind of an artificial substitute for gold and since I never buy any gold, I never buy any bitcoin. I recommend that other people follow my practice." "[The Daily Journal] will not be following Tesla into bitcoin." Tesla and Bitcoin Munger was asked to choose which was more ridiculous, bitcoin trading at $50,000 or Tesla's fully diluted enterprise value of $1 trillion. He quoted author Samuel Johnson, who when presented with two choices, said, "I can't decide the order of precedency between a flea and a louse." "I feel the same way about those choices," Munger said. "I don't know which is worse." Banks "Banking, run intelligently, is a very good business. The kind of executives who have a Buffett-like mindset and never get in trouble are a minority group, not a majority group." "It's hard to run a bank intelligently. There's a lot of temptation to do dumb things which will make the earnings next quarter go up, but are bad for the long term." Wells Fargo "There's no question that Wells Fargo has disappointed long-term investors like Berkshire. The old management were not consciously malevolent or thieving, but they had terrible judgment in having a culture of cross-selling, with incentives on the poorly paid employees that were too great to sell stuff the customers didn't really need. "When the evidence came in that the system wasn't working very well because some of the employees were cheating some of the customers, they came down hard on the employees instead of changing the system. That was a big error in judgment. It's regrettable." "You can understand why Warren [Buffett] got disenchanted with Wells Fargo I'm a little more lenient. I expect less out of bankers than he does." BYD "BYD stock did nothing for the first five years we held it and last year it quintupled. What happened was that BYD is very well-positioned for the transfer of Chinese automobile production from gasoline-driven cars to electricity-driven cars." "It's in a wonderful position and that excited the people in China - which has its share of crazy speculators - and so the stock went way up." Selling Overvalued Stocks "I so rarely hold a company like BYD that goes to a nosebleed price, that I don't think I've got a system yet. I'm just learning as I go along." Costco "It's been amazing that one little company, starting up not all that many decades ago, could become as big as Costco did, as fast as Costco did. Part of the reason for that was cultural. They have created a strong culture of fanaticism about cost and quality and efficiency and honor, all the good things, and it's all worked." "People really trust Costco to deliver enormous values and that is why Costco presents some danger to Amazon. They've got a better reputation for providing value than practically anybody, including Amazon." Value Investing "Value investing, the way I conceive it, is always wanting to get more value than you pay for when you buy a stock. That approach will never go out of style." "All good investing is value investing. It's just that some people look for value in strong companies and some people look for value in weak companies." Amazon Founder Jeff Bezos "I'm a great admirer of Jeff Bezos, whom I consider one of the smartest businessmen who ever lived." Alibaba Founder Jack Ma "Jack Ma was very arrogant to be telling the Chinese government how dumb they were and how stupid their policies were and so forth. Considering their system, that is not what he should have been doing." The Pandemic Enriching the Wealthy "We were trying to save the whole economy under terrible conditions. We made the rich richer not as a deliberate choice; it was an accidental byproduct of trying to save the whole civilization. It was probably wise that we acted exactly as we did." Modern Monetary Theory "So far, the evidence would be that maybe the modern monetary theory is right. Put me down as skeptical." Inequality "I'm way less afraid of inequality than most people who are bleating about it. Inequality is absolutely an inevitable consequence of having the policies that make a nation grow richer and richer and elevate the poor. I don't mind a little inequality." Politics Munger bemoaned the rising amount of "hatred and irrationality" in politics, but argued the country had been well-governed for the past century. "The system of checks and balances and elections that our founders gave us, actually gave us pretty much the right policies during my lifetime, and I hope that will continue in the future." The Evolution of Business "Long-term business success is a lot like biology. In biology, the individuals all die and eventually so do all the species. And capitalism is almost as brutal as that." "Think of what's died in my lifetime. Who ever dreamed when I was young that Kodak and General Motors would go bankrupt? It's incredible what's happened in terms of the destruction." Lifelong Learning "I think I had the right temperament. When people gave me a good idea, I quickly mastered it and started using it and just used it for the rest of my life. It's such a simple idea. Without the method of learning, you're like a one-legged man in an ass-kicking contest." Psychology "It's one of the most ignorant professions in the world," Munger said, highlighting that many psychologists fail to connect their theories and insights with other types of knowledge. Adapting to Technological Change "If you have a fixable disadvantage, remove it, and if it's unfixable, learn to live without it. What else can you do?" Challenging One's Beliefs "I'm not really equipped to comment on a subject until I can state the arguments against my conclusion better than the people on the other side. If you're looking for disconfirming evidence, that's a good way to help remove ignorance." "When we shout our knowledge out, we're really pounding it in, we're not enlarging it." Early-Stage Investments "Warren and I are better at buying mature industries than we are at backing startups. I would hate to compete with Sequoia in their field, they would run rings around me." "I got close to Sequoia when, with Li Lu, we bought into BYD. We were buying into a venture-capital-type investment, but in the public market. With that one exception, I've stayed out of Sequoia's business because they're so much better at it than I would be." The Queen's Gambit and Investing "I have seen an episode or two. What I think is interesting about chess is to some extent, you can't learn it unless you have a natural gift. And even if you have a natural gift, you can't be good at it unless you start playing at a very young age and get huge experience." "Any intelligent person can get to be pretty good as an investor and avoid certain obvious traps, but I don't think everybody can be a great investor or a great chess player." Do Managers Have a Moral Responsibility to Have their Shares Trade as Close to Fair Value as Possible? "I don't think you can make that a moral responsibility because if you do that, I'm a moral leper. The Daily Journal stock sells way above the price I would pay if I were buying a new stock." "The management should tell it like it is as all times and not be a big promoter of its own stock." Oil and Gas "The oil-and-gas industry will be here for a long, long time even if we stop using many hydrocarbons in transportation. The hydrocarbons are also needed as chemical feedstocks. I'm not saying that oil and gas is going to be a wonderful business, but I don't think it's going away." Wealth and Happiness "Most people are born with a happy stat, and their happy stat has more to do with their [inherent] happiness than their outcomes in life," Munger said. He argued that most people wouldn't be significantly happier if they were richer or much more miserable if they were poorer. Physics and Investing "I don't use much physics in solving my investing problems. Occasionally some damn fool will suggest something that violates the laws of physics, and I will always turn off my mind the minute I realize the poor bastard doesn't know any physics." Marriage "A little wisdom in spouse selection is very desirable. You can hardly think of a decision that matters more to human felicity than who you marry." Creativity in Old Age "I don't have any wonderful new thoughts. To the extent that my thoughts have helped my life, I've pretty well run the course. I don't think I'm likely to have any new thoughts that are going to work miracles either. But I find that the old ways of doing things still work. I'm kind of pleased that I'm still functioning at all. I'm not trying to move mountains." Secrets to a Long, Happy, and Healthy Life "I'm alive because of a lucky genetic accident. I don't have any secrets. I think I would have lived a long time if I'd lived a different life." "The first rule of a happy life is low expectations. If you have unrealistic expectations, you're going to be miserable all your life. Also, when you get reverses, if you just suck it up and cope, that helps more than if you just fretfully stew yourself into a lot of misery." Rose Blumkin [of Nebraska Furniture Mart] had quite an effect on the Berkshire culture. Her mottos were, 'Always tell the truth' and 'Never lie to anybody about anything.' Those are pretty good rules and they're pretty simple." Life After the Pandemic "When the pandemic is over, I don't think we're going back to just the way things were. We're going to do a lot less travel and a lot more Zooming. The world is going to be quite different." -Paul R. Ross, CFA  Does the thought of plowing money into a start-up company or buying shares of a company that recently went public excite you? Are you enticed by high-risk/high-return investments? Or do you prefer the "sure thing," believing that slow and steady can win a lot of races? If so, you might be considered a more risk-averse investor. There is no right or wrong type of investor, just what's right for you. Most people fall somewhere in between these two extremes. But knowing what your needs are, and what type of investor you are, can help get a sense of your risk tolerance and ultimately help you invest in a way that will build wealth over time. Like a finger print is unique to each individual, no two people will have the same views on investing. In less than 2 minutes, you can find out where you stand, are you a Tortoise or a Hare? Mark the responses below after each sentence that best describe your immediate reaction to each of the following statements. Try not to overthink your answers.  Score yourself below.  Drum roll please... Whatever your score, be it 8 or 40, or somewhere in between, knowing this number is critical to your investing success. Knowing your comfort level will go a long way in determining what type of investments are suitable for you and which ones are not. Investors would be wise to follow the ancient Greek aphorism "nosce te ipsum," more commonly known as "know thyself." -Paul R. Rossi, CFA For a deeper dive into your risk tolerance and to see if your investment/retirement portfolio is correctly aligned with who you are, click here.  One of the fundamental laws of the universe, is the Law of Gravity. Einstein taught us that gravity is the bending of space/time, which we perceive as objects being drawn toward each other. Finance's "Law of Gravity" is the idea of the relationship between risk and return. The idea is pretty straight forward: The riskier the investment, the potential greater the return. Said another way, the lower the risk, the lower the expected return. The relationship between risk and return is positivity correlated, therefore the more an investor is willing to dial up their risk, the more return they expect to make. Let's take two relatively straight forward examples which will clearly reveal the gravity law in finance. Low Risk example: Putting your money in your local FDIC insured bank is a extremely safe investment. In a nut shell, there is next to no chance that you will lose your principal amount (up to the FDIC limit of course). For this ultra safe investment, investors today are earning between 0.0% - 0.50% (annually). Keep in mind, when you factor in inflation, this 'safe' investment actually loses purchasing power over time - but this for another conversation (read here) which talks about inflation and its effect on purchasing power. High Risk example: Taking this same money out of your bank and placing all of it on one hand of Black Jack at your favorite casino. The risk is extremely high that you will lose all of your money on that single bet, however, there is a chance that you will 'win' your bet and double your money in an extremely short period of time - a great return over an extremely short period of time. So this high risk action has the potential of high returns. So next time you hear of an investment opportunity that sounds 'too good to be true,' take a minute to think of the simple relationship that return = risk. -Paul R. Rossi, CFA The 10-Year Treasury is down over 59% AND is up over 94%. How is this possible? If you measure over the last 3 years, the 10-Year Treasury is down 59%. If you measure over the last 6 months the 10-Year Treasury is up over 94%.   Time frames matter.

-Paul R. Rossi, CFA  “It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way.” – Charles Dickens, the famous opening quote from the 1859 book, A Tale of Two Cities. Eerily, this quote sounds like it could have been written yesterday. At one point, A Tale of Two Cities was cited as the best-selling novel of all time. Dickens was a champion of the poor in his writings and in his life as he became the most popular novelist of his time. Astoundingly, his works have never gone out of print. Growing up in England he lived in poverty, leaving school as a young boy to work in a factory to help support his family due to his father continually living beyond his means. His father eventually went to debtors' prison. Looking at his early life, most would never have predicted who he would eventually become, and the impact he would have. Looking back over the past 10-years, for some investors, it was as Dicken’s wrote, it ‘was the season of Light…it was the best of times.” What have the 5 best performing companies in the S&P 500 done over the last 10 years? The top 5 performing stocks were:

Doing a thought experiment, investing $10k into each company 10-years ago would have turned this combined $50,000 investment into over $2,800,000. A gain of 5,752% gain. It truly was, “the best of times” for these investors. Conversely, how did the 5 worst performing companies in the S&P 500 do over the last 10 years?

Investing $10,000 into each of these companies would have turned the $50,000 investment into less than $12,000, losing -$38,000. A whopping loss of -75% and a difference of over $2,838,000 in terminal wealth between these two investors. For these investors, “it was the worst of times.” What can we learn from this? Different investors can experience wildly different returns. Investing can be extremely rewarding and horribly painful over the exact same time-period. -Paul R. Rossi, CFA  The financial services industry and in particularly the investment and portfolio management sub-field has a quite a few industry specific terms. As a group, financial professionals tend to think most people who are not in our industry understand many of terms we use so freely - which of course isn't necessarily true. So I've attached a link to a great resource of financial glossary terms provided by YCharts.com. If you are an avid financial reader or DIY investor you might want to book mark this page, and then when you come across a term you aren't sure about, you'll now have a way to bring yourself up to speed. The link is at the very end of this article. From the several hundred definitions provided, here are a couple of examples, taken directly from the financial glossary (Altman Z-Score and Beta) at YCharts.com: ALTMAN Z-SCORE CAUTION: The Altman Z-Score is meant to be applied only to manufacturing firms that are near bankruptcy. It was not based on a sample including non-manufacturing firms (service firms, banks, etc.). Use it at your own risk with those companies, but beware that bankruptcy probabilities may be misstated. The Altman Z-Score helps investors to gauge the probability of a company going bankrupt. Generally, firms with a score above 3.00 have a low probability of bankruptcy, and those with a Z-Score of less than 1.81 have a relatively high probability of bankruptcy. Note that this is a probabilistic model, so it will not classify perfectly. The score was first published in a 1968 paper by Edward Altman titled "Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy." Altman re-tested the model in a 2000 paper titled "Predicting financial distress of companies: Revisiting the Z-score and Zeta models". The paper showed that the model still had utility for looking at manufacturers, though the number of misclassifications did increase over time. FormulaZ = 1.2 x (Working Capital / Total Assets) + 1.4 x (Retained Earnings / Total Assets) + 3.3 x (Earnings Before Interest and Taxes / Total Assets) + 0.6 x (Market Value of Equity / Total Liabilities) + 1.0 x (Sales / Total Assets) Where: Working Capital = Current Assets - Current Liabilities Market Value of Equity = Market Cap + Preferred Stock BETA Beta is a measure of the risk of a stock when it is included in a well-diversified portfolio. In financial theory, the Capital Asset Pricing Model (CAPM) breaks down expected stock returns into two components. The first is the return that would be expected based on covariance with the movements of the market (for most stocks, when the market as a whole goes up, the price of the stock will also go up). This is considered systematic risk. The second part is the increase in the price of a stock that is not explained by the market (nonsystematic risk). The first part - covariance with the market - is what Beta captures. When Beta is positive, the stock price tends to move in the same direction as the market, and the magnitude of Beta tells by how much. If a stock's Beta is greater than 1, that means that when the market index goes up 1%, we expect the stock will go up by more than 1%. On the contrary, if the market goes down by 1%, we expect the stock to go down by more than 1%. Negative betas signify a negative correlation. When the market goes up, a stock with a negative beta would be expected to go down. For readers with a background in regression analysis, Beta is the slope of the linear regression shown in the formula below, where Returns are the return on an individual stock or portfolio, R_f is the risk free rate, R_Market is the return on a market portfolio, and e is an error term. So take a look around and enjoy a great resource from the YChart.com website. Click the link below. -Paul R. Rossi, CFA Financial Glossary (ycharts.com)  So, it’s that time of year (again). In the spirit of making predictions that will actually come true, here are our Top 10 predictions in order of certainty. In other words, Prediction #10 is pretty-darn-certain to happen while Prediction #1 is absolutely guaranteed.

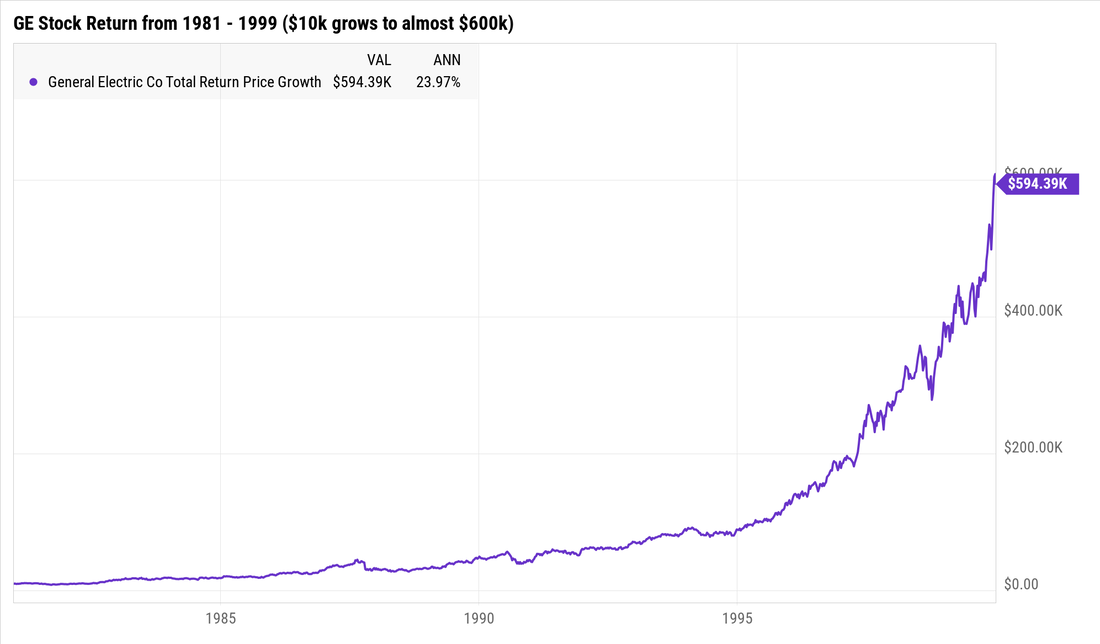

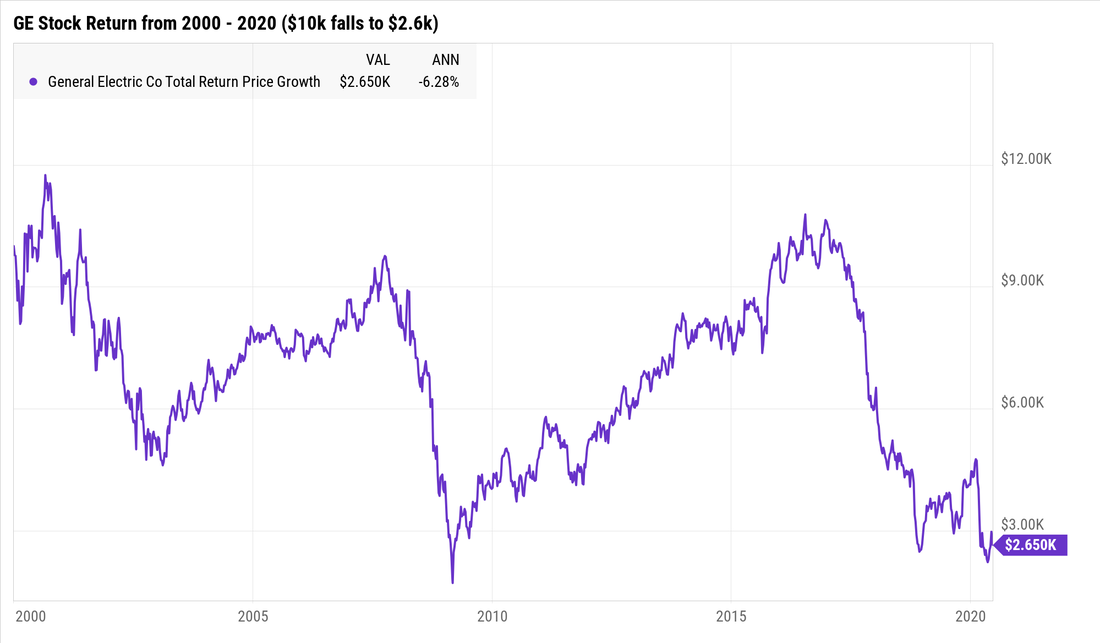

#10. Stock Market Volatility Will Continue The stock market, the bond market, the commodities markets, the geopolitical landscape, pretty much all endeavors where people are involved are volatile – some more than others. This is a feature not a bug. #9. Sectors Will Rotate The S&P 500 has eleven sectors (technology, financial, real estate, health care, etc.), and guess what? Various sectors fall in and out of favor and therefore their returns will be all over the map. Market prognosticators will give a reason as why this happened...but always after-the-fact. #8. Congress Will Continue To Be a Lightning-Rod Why? Because 535 people come from all over the country having all different agendas. However, the one agenda they all share is wanting to get reelected. #7. The Business Media Will Continue To Talk About What The Fed Is Going To Do Next Economists enjoy talking about when the Fed is going to lower or raise short-term interest rates. Why? Because it gives people the idea that some so called experts know what the Fed is going to do - the secret is, they don't. Predicting almost anything related to the economy is next to impossible. My advice is to get comfortable being uncomfortable. #6. There Will Be Earnings Disappointments Some companies will do worse than expected. Some will even go out of business. Some will disappoint and then surprise in the future. #5. There Will Be Earnings Surprises Some companies will do better than expected. Some of these companies will buy other companies. Trying to predict which companies will continue to do well is harder than understanding quantum mechanics. Capitalism is fierce, tread lightly. #4. The Housing Market Will Change Mortgage rates, lending standards, building permits, and employment all effect the housing market, and these 4 inputs are always changing so it’s nearly impossible for housing not to change. #3. The U.S. Dollar Will Fluctuate Many factors affect the movement of the U.S. dollar and it's virtually impossible to predict the direction, but many will try. Don’t be one of them. #2. Patient Long-Term Investors with a Well-Thought Out Plan Will Do Well Past performance of course will not guarantee future results, but it is a pretty-good indication of what the range of outcomes will likely be. #1. My team Will Continue To Serve You In a Fiduciary Capacity As always, we believe that making decisions based on evidence rather than predictions will give you the best odds of success. Together, we will help plan, build, and execute a financial roadmap that will allow you to live on purpose. And that is one prediction that is absolutely guaranteed. -Paul R. Rossi, CFA Founded in 1892, General Electric has been around for over 128 years and the company has built and produced an amazing array of products from light bulbs, to jet engines, to magnetic resonance Imaging (MRI) machines, and almost everything in between during various periods of time. Understandably, many business school students and investors have studied, analyzed, and marveled over GE's long-term success. You can see below that a $10,000 investment in GE back in 1981 grew to almost $600,000 in less than 20 years. This is truly an amazing record and something very few companies achieve. In fact, the +20% annualized returns that GE produced over that time period are very similar to the returns Apple has produced from 2000-2020. Quite astounding to say the least.  But even with all its success, both for consumers and its shareholders, no company is immune to the extremely competitive business world. Like every global company today, GE competes in the most competitive arena the world has to offer, that arena is called Capitalism. Capitalism is fierce. And as such, the story changes dramatically for people who invested in GE anytime over the last 20 years. See the chart of GE below (2000 - 2020). GE has been dead money for two decades. Especially if you review how well the overall stock market performed during that same time period. $10,000 invested in GE back in 2000, an investor lost a whopping 7,400, leaving only $2,600. During this same time period, that same $10,000 invested the overall stock market grew to over $30,000.  As much as you, stock market analysts, Forbes, or your neighbor loves a particular company, even the most successful companies, some with 100+ year old track records might not provide good returns going forward. Sometimes history isn't a guide to the future and back in 2000 it wasn't for GE.

Understanding where a company competes, what are its biggest threats, what the business landscape looks like, determining their competitive advantage, answering another 100 or so difficult questions, and then properly being able to determine its value is paramount to having a chance of investing success. Ask yourself, back in 2000 after GE's amazing growth, wouldn't you have thought GE would continue to do well for the next 20 years? Competition is fierce, tread lightly.  illustration by Tim Sheaffer Mike Tyson famously said, “Everyone has a plan until they get punched in the mouth.” The brutal “punch in the mouth” brought on by Covid-19 caused markets worldwide to collapse and the repercussions sent shock waves throughout our daily lives. It’s changed how we work, learn, shop, eat, interact and generally how we live. Having a plan is one thing (and albeit it a very important thing) but being able to stick to a well-thought-out plan is equally important, as Iron Mike Tyson’s quote implies. If you were not sure before 2020, markets are volatile and can move extremely fast. It's best to think that we will get punched in the face from time to time and plan accordingly. So how do we make sure our emotions don’t get in the way of our best judgement when we are getting punched in the face? The best time to build a resolute plan is prior-to, not during the barrage. A plan that anticipates getting punched in the face. Why do we want to do this? Because our minds can be our own worst enemy under duress and we don't want to change our plan when getting punched in the face. Several years ago Daniel Kahneman, the 2002 Nobel prize winning economist wrote about System 1 and System 2 thinking in his seminal book, “Thinking, Fast and Slow.” He describes how System 1 thinking helps us make everyday decisions and react quickly when we need to, while System 2 thinking helps us make more purposeful decisions and work on more complicated tasks. For both System 1 and System 2 thinking, our minds try to save energy by using heuristics to make decisions more efficiently. And most of the time this works fine, but biases can pop up which can lead us astray - these biases can do real damage when we don't even realize they are behind the scenes causing havoc. The challenge is to understand the biases we may have, the even bigger challenge is understanding the biases we don’t even know we have that are influencing us. Psychologists and behavioral scientists have researched and documented well over a hundred and fifty different biases that can lead us astray when making decisions. We’ll discuss just a few biases that are particularly damaging when it comes to investing.

If you said yes, you are not alone. 90% of all drivers in a famous study of everyday people said they were above-average drivers - myself included. Unfortunately, basic math tells us this isn't possible. This is overconfidence bias. We all tend to be unrealistically optimistic about our chances of success and our abilities. When it comes to making investing decisions, this can result in investors thinking they can outsmart the market. This type of thinking leads people to believe they have a superior edge when in reality they do not.

Quickly Putting It All Together: Here are a few things you can do to help make the best (System 2) decisions possible and overcome those nasty biases and unrelenting emotions.

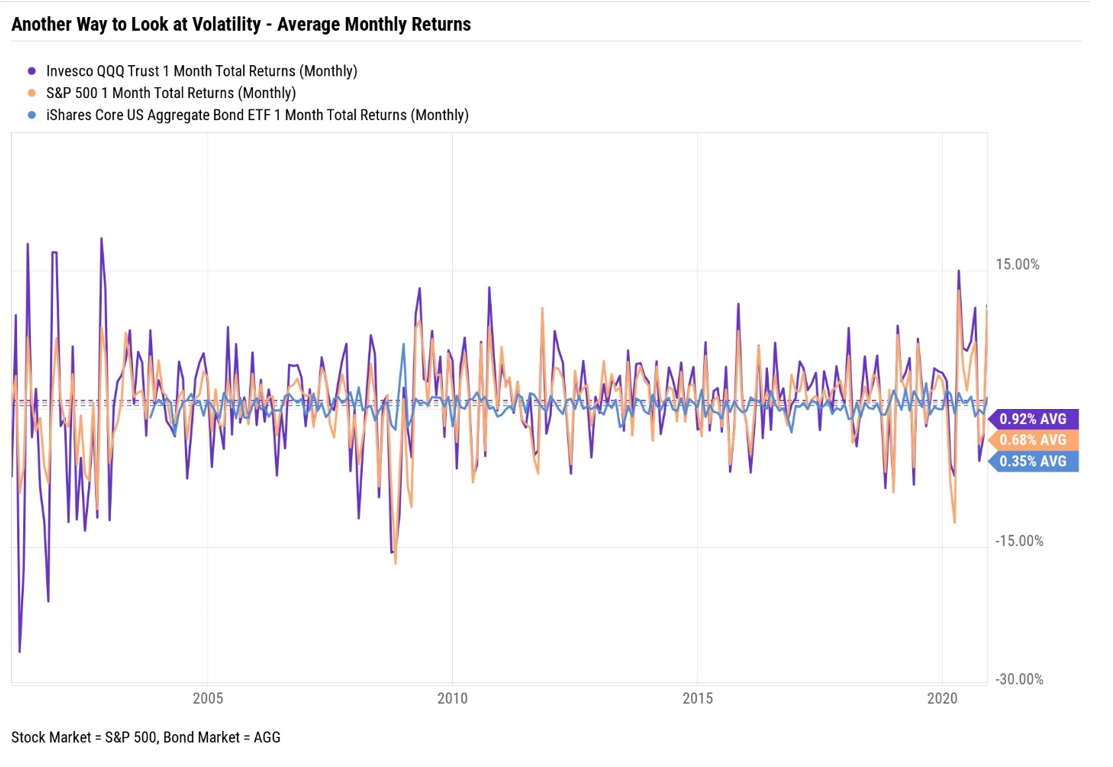

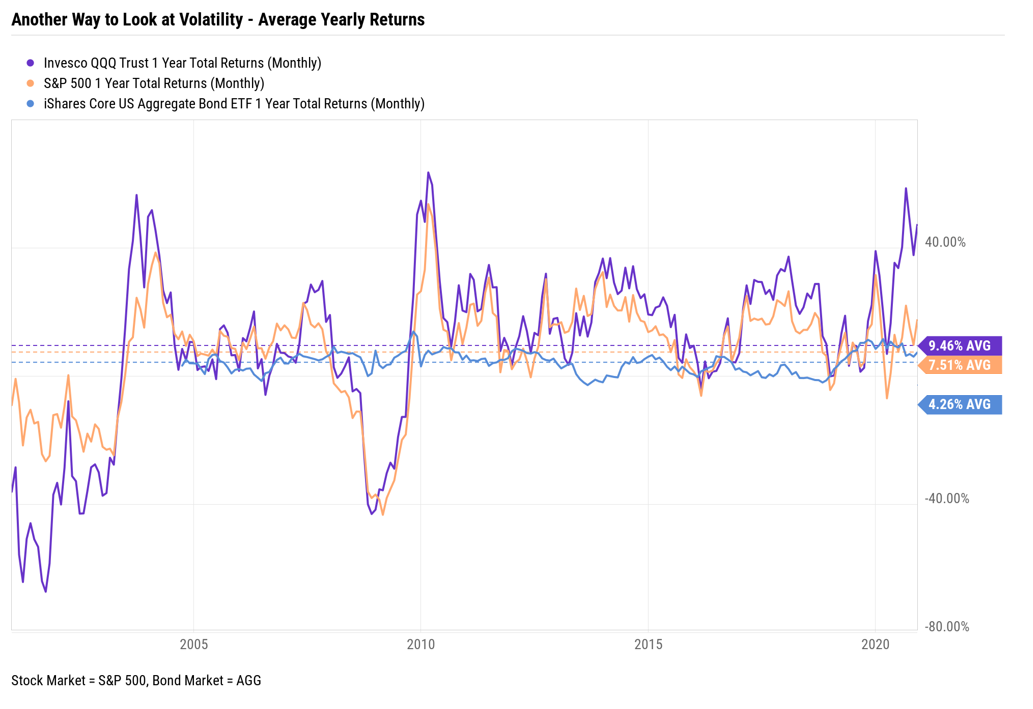

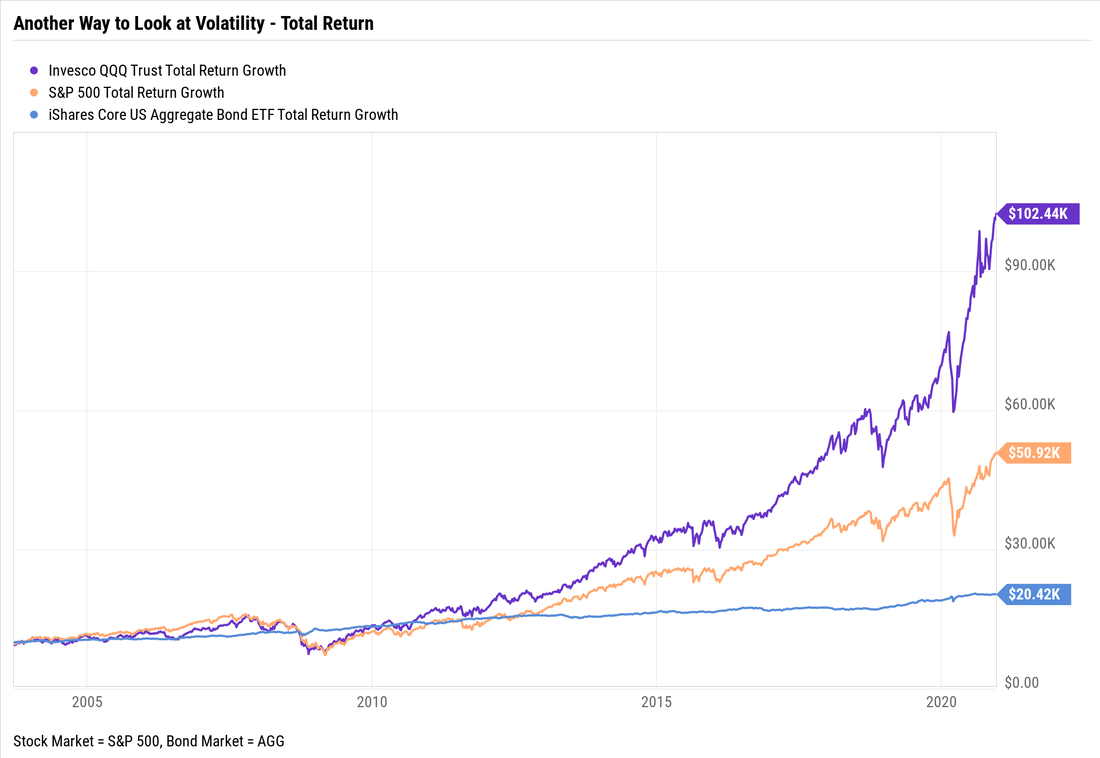

Cheers to an emotional and bias free investing future! -Paul R. Rossi, CFA  What is an IPO? An IPO (Initial Public Offering) is when a private company transitions from being a private company to public company and it's at this point in time that Joe and Jane public can for the first time invest and own shares of the company. By nature, IPOs are risky. Why? Well investors have relatively limited financial history on the company going public. Why? Because many private companies are smaller and don't have a long track record and prior to "going public," the private companies are not required to have audited financial statements. So how does anyone know which companies are good buys and which ones will turn out to be bad investments? Good question...and a very tough question. What should you look for when evaluating a new IPO? Interestingly enough, similar analysis should go into an IPO and a company that is already public. Things like understanding their financial situation by analyzing their balance sheet, income statement, and cash flow statement. You should know the various financial ratios (Quick Ratio, Debt/Equity Ratio, Conversion Ratio, ROE, etc.) and how these ratios have been trending over time. Are they getting better or worse? You should understand the various drivers that will impact the company - both good and bad. What is the company's (TAM) Total Addressable Market? Who are their biggest competitors? What is the company's advantage and is their advantage sustainable? What Warren Buffett calls this a company's "durable competitive advantage." And after you've thoroughly read through the company's prospectus (including the foot notes), answered an additional 101 questions or so, you can then move on to trying to value the company. While there are several ways, from Price/Sales, Price/Earnings, Price/EBITDA, to name a few, generally the most robust way is to do a comprehensive discounted cash flow analysis (DFC). A DFC is a process that uses the projected future cash flows of the company into perpetuity and discounting them back based upon current risk and interest rate levels. Once you have this DFC you can then stress the results by changing various assumptions, like initial cash flows, growth rates, and discount rates to see how the valuation changes. So build a DCF, then take these various DFC valuations and compare this with the IPO valuation to see if buying into this company make sense. What makes buying an IPO even more difficult to evaluate is the fact that many of them don't have positive cash flow. So how do you value a company that doesn't make money? Again, another great question and another difficult one. The big driver will be the assumptions used in what the company might look like in several quarters or even several years down the road. So playing fortune teller becomes a necessary requirement. Something, I'm typically not a fan of. Uggg. So having read all this, while history is never an accurate forecast of the future, sometimes it can provide valuable sign posts with which to gain some insight. If you have a high tolerance for taking big risks then maybe allocating a portion of your investment portfolio to IPO's might be for you. However it would be prudent to understand and recognize that buying IPO's is the quintessential, "buyer beware" transaction. -Paul R. Rossi, CFA The Stock Market is Volatile. It's volatile on a daily basis. It's volatile on a monthly basis. And it's volatile on a yearly basis. Take a look at the first two charts below which show the 20-year period of monthly and yearly returns respectively for: